Mintos Review Summary

Mintos remains the leading P2P investment platform in Europe, but it doesn’t always succeed in protecting investors’ interests. If you choose to invest, prior experience with P2P lending is essential, along with the discipline to select only the strongest loan originators.

The KPIs of top lenders on Mintos are potentially appealing and can offer good opportunities for those who know how to assess them.

Key takeaways from our Mintos review:

- Lower historical return than on other platforms

- Broad diversification options

- Many new lenders from emerging markets

- Only suitable for experienced P2P investors

If you are considering joining Mintos, you should conduct thorough due diligence on their lending companies before investing your money.

Our Opinion of Mintos

Our assessment focuses mainly on Mintos’ P2P lending marketplace, rather than its newer investment products like bonds, ETFs, or real estate.

Mintos was originally created to fund the lending portfolios of its own shareholder companies. Over time, it expanded into a broader P2P platform, but not without challenges. Millions of euros remain tied up in defaulted lenders who failed to honor buyback guarantees, leaving many investors with funds stuck in recovery for years.

Loan performance has shown some improvement in 2024–2025, but liquidity issues such as pending payments remain a recurring problem.

While Mintos promotes its regulatory status in Latvia, this has not materially increased investor protection. That said, Mintos still hosts some loan originators with the strongest KPIs in the industry, including solid debt-to-equity and equity-to-assets ratios.

For experienced investors willing to research and carefully select the best lenders, Mintos can still offer attractive returns of up to 21% per year.

Beyond loans, Mintos now offers additional products:

- ETFs – Suitable for beginners who don’t want to research ETFs or manage exposure selection.

- Real estate – Should be approached with caution due to long loan terms and limited liquidity.

- Bonds – Can provide a reasonable balance between risk and return.

However, for passive investors seeking a simple, low-maintenance option, Mintos’ risks, liquidity concerns, and ongoing recovery issues make it a challenging fit.

What Is Mintos?

Mintos is a Latvian multi-asset investment platform that has become one of the most popular choices for European investors. The platform is best known for providing access to diversified loan portfolios from a wide range of international loan originators.

In addition, Mintos offers investment options in ETFs, bonds, and real estate products, giving investors broader exposure beyond loans.

In this Mintos review, we examine how the platform operates, the risks and returns associated with each product, and whether Mintos is a safe and worthwhile investment. We also highlight the main pros and cons that every investor should consider before signing up on Mintos.

Pros

- The biggest P2P lending marketplace in Europe

- A wide variety of loans

- Regulated in Latvia

- Higher yield for newly joined investors

- No cash drag

Cons

- Unreliable buyback guarantee

- Many suspended lenders

Mintos Bonus

With our Mintos promo code, you can receive a €25 bonus after registering with our link and investing funds until the end of the bonus period.

Requirements

To invest on Mintos, you’ll need to fit with a couple of their requirements, such as:

- Be over 18 years old

- Have a European bank account in your name

- Don't reside in the UK

- Pass the KYC requirements

- Pass the suitability and appropriateness test

Remember that if you don't pass the suitability test, which tests your knowledge in the P2P lending space, you won't be able to use some of the critical functions of Mintos, like the Mintos strategies.

No EUR bank account? No problem

- 💳

You can fund your Mintos account in nine different currencies, but the most cost-effective option is to transfer your money in EUR. This way, you avoid unnecessary conversion fees. While Mintos does allow you to invest in multiple currencies, keep in mind that this exposes you to foreign exchange risk.

Another important detail: Mintos can disable its internal currency exchange feature at any time. If that happens, you won’t be able to convert your investments back to EUR before withdrawing, which may limit your flexibility. For most investors, the cheapest and most reliable method to deposit funds into Mintos is through a SEPA transfer.

If you are based in the UK and want to invest in European P2P lending platforms, check out our in-depth reviews of Fintown and PeerBerry, as Mintos currently does not accept UK investors.

Risk & Return

Mintos advertises annual returns ranging from 3% to 21%, depending on the product you invest in. However, higher yields come with higher risks. In the case of loan investments, Mintos has historically carried more risk compared to many other P2P lending platforms.

While attractive cashback campaigns can boost potential returns, investors should be aware that over 20% of the current loan portfolio is underperforming.

This can significantly reduce the real returns, even for well-diversified portfolios. With that in mind, let’s take a closer look at the risk factors and explore the different investment products available on Mintos.

Investments in Loans

Mintos has transitioned from offering claim rights to issuing Notes (asset-backed securities) as part of its move towards becoming a fully regulated investment firm.

Previously, before receiving its brokerage license, investors could buy into individual loans starting from €10, secured by a claim right through a loan assignment.

Today, Mintos structures investments differently by pooling together multiple similar loans into a single Note. Each Note is recognized as a financial instrument and comes with its own ISIN (International Securities Identification Number).

The minimum investment amount has increased to €50 per Note, with each Note typically consisting of 6 to 20 loans.

Below, we break down the simplified process of issuing Notes on Mintos.

With the introduction of Notes, the return structure remains the same as under the previous setup. Investors continue to earn interest generated by the underlying loans. In terms of protection, Mintos relies on the lending companies to offer a buyback guarantee.

This means that if a loan is delayed for more than 60 days, the loan originator is expected to repurchase your investment. However, this mechanism should not be seen as a reliable safeguard. History has shown that several lending companies on Mintos have failed to honor their buyback obligations, leaving investors exposed to significant risk.

€20,000 Protection Scheme

As a regulated firm in Latvia, the government provides €20,000 investor protection for investors' uninvested funds on Mintos. This means that if Mintos goes bankrupt and you have uninvested funds, Latvia will reimburse you up to €20,000.

This "scheme" doesn't cover your active investments on the platform, and Mintos pointed out that it should not be interpreted as a "deposit insurance."

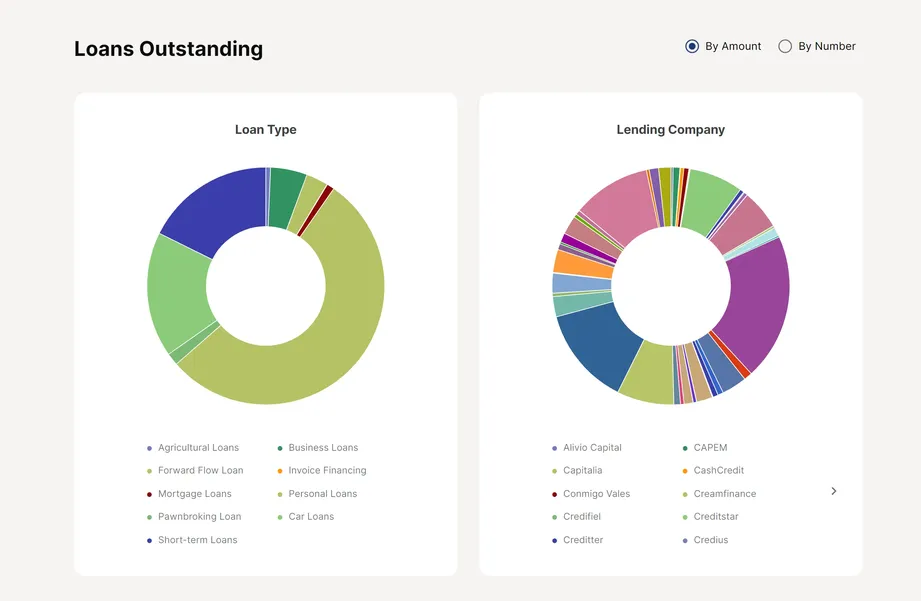

Loan Types

While Mintos promotes various loan types, most loans bundled into Notes on Mintos are short-term, personal, or car loans.

Almost two-thirds of loans on Mintos are short-term loans, otherwise known as micro or payday loans.

Those loans usually have a short-term max. 90 days.

Note that short-term loans are riskier than mortgage-backed loans, as default rates can be as high as 40%, depending on the country and lending company.

Mintos also lists mortgage, business, and agricultural loans, as well as invoice financing. Those loan types are, however, barely available. If you are looking for investments in secured loans, you might want to read our review of LANDE.

Diversification Options

Mintos’ popularity is largely driven by the wide variety of loan originators available on the platform. In theory, investors can access over 51 loan originators across 31 countries.

However, it’s important to understand that many of these lenders belong to larger financial groups, which increases concentration risk. Due to this structure, the performance of one loan originator is often correlated with that of others in the same group.

If a single lender defaults, it can trigger financial stress across the group, exposing investors to additional risk. Many of these groups operate multiple lending companies in developing markets, where the risks are generally higher.

While Mintos frequently promotes “group guarantees” as a safety net in the event of default, history shows that this mechanism does not always work effectively. A well-known example is the suspension of Varks in Armenia, which also led to the collapse of the Finko Group, despite its group guarantee.

Another concern for investors is the potential conflict of interest on Mintos. Several lending partners share the same shareholders as Mintos itself, and the platform funds a significant number of payday loan providers owned by these shareholders.

This overlap raises questions about transparency and could harm investor confidence. Looking at historical performance, more than 50% of all “funds in recovery” are linked to lenders connected to Mintos’ shareholders, a concern that investors should carefully consider before allocating capital.

Buyback Obligation

Another important feature on Mintos is the so-called buyback obligation. If you invest in loans with this feature, the lending company is supposed to repurchase your investment once the loan is delayed for more than 60 days.

In practice, however, this obligation often works more like a promise than a guarantee. Many lending companies on Mintos have failed to honor their buyback commitments in the past. What’s more, loan originators can use this mechanism to their advantage.

Instead of activating the buyback, they can simply extend the loan term, sometimes by as much as six months. By doing so, they avoid triggering the obligation, but your money remains locked, reducing your liquidity and flexibility as an investor.

This tactic isn’t unique to Mintos. Similar practices have been observed on Lendermarket and, to some extent, VIAINVEST, particularly during periods when investor funding volumes decline.

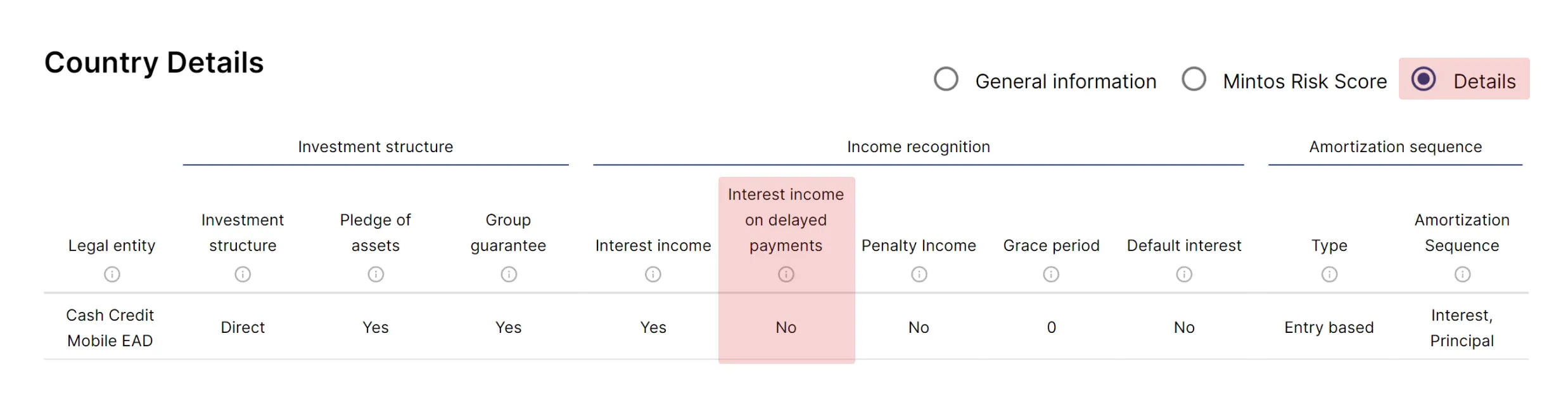

No Interest on Delayed Payments

Not all lending companies on Mintos pay interest on delayed loans. This means that if your investment in Notes is late, you may earn no interest during the delay period—directly reducing your overall return while increasing your risk exposure.

Before investing, it’s crucial to check whether the loan originator compensates investors for late payments. You can verify this on the Loan Originator Page by scrolling down to “Country Details” and enabling the “Details” view.

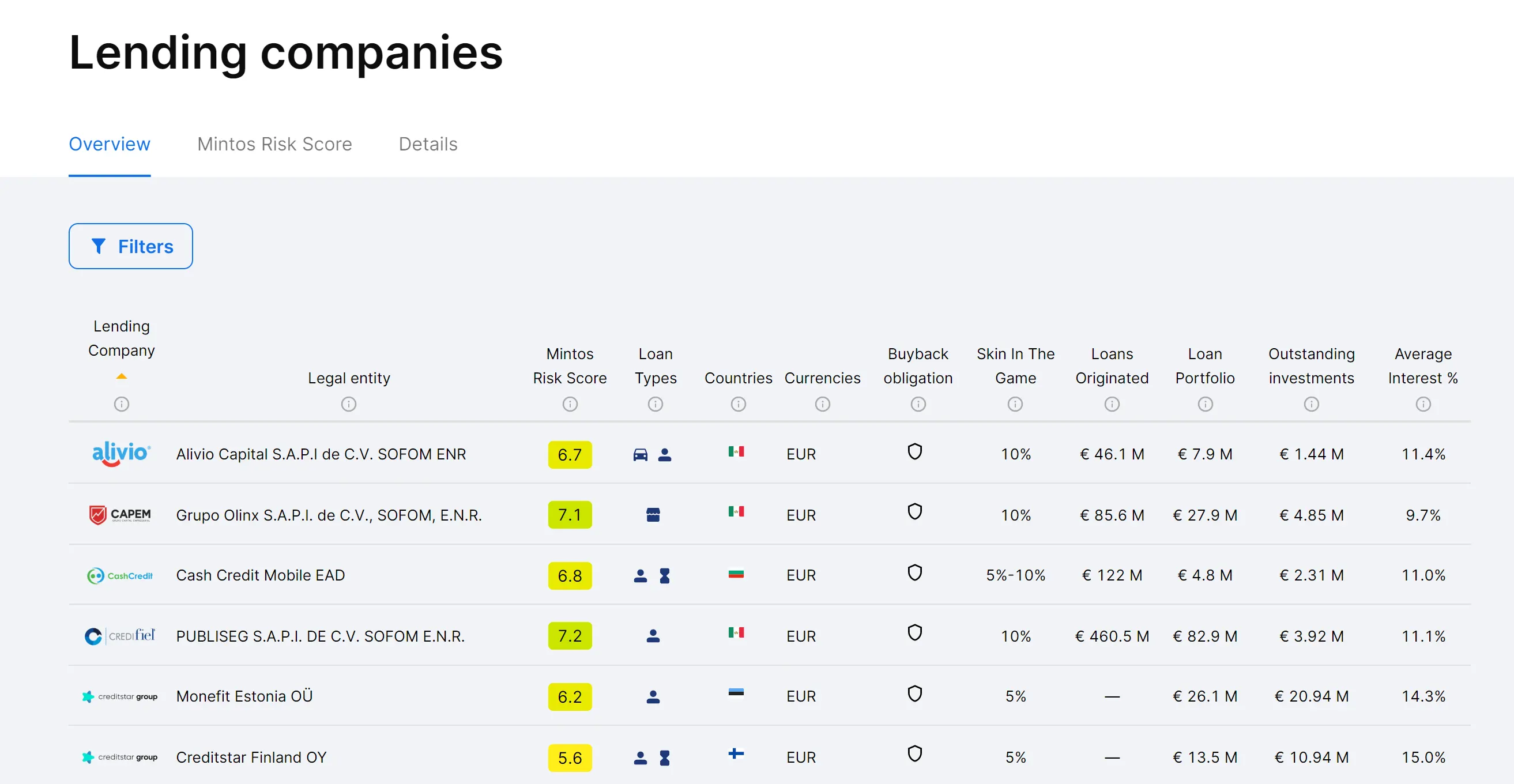

Mintos Loan Originators

One of Mintos' users' favorite features is the loan originator section.

Few P2P lending platforms give you as many details about their loan originators as Mintos. You can learn about the following:

- Skin in the Game (how much of its own money the lending company is investing in its loans)

- Mintos' Risk Score (how well-rated is the lending company)

- Countries

- Loan types

- Currencies

- Portfolio performance (limited)

- The company’s financial reports

You can analyze every loan originator or exclude countries, automatically eliminating loan originators operating in high-risk locations.

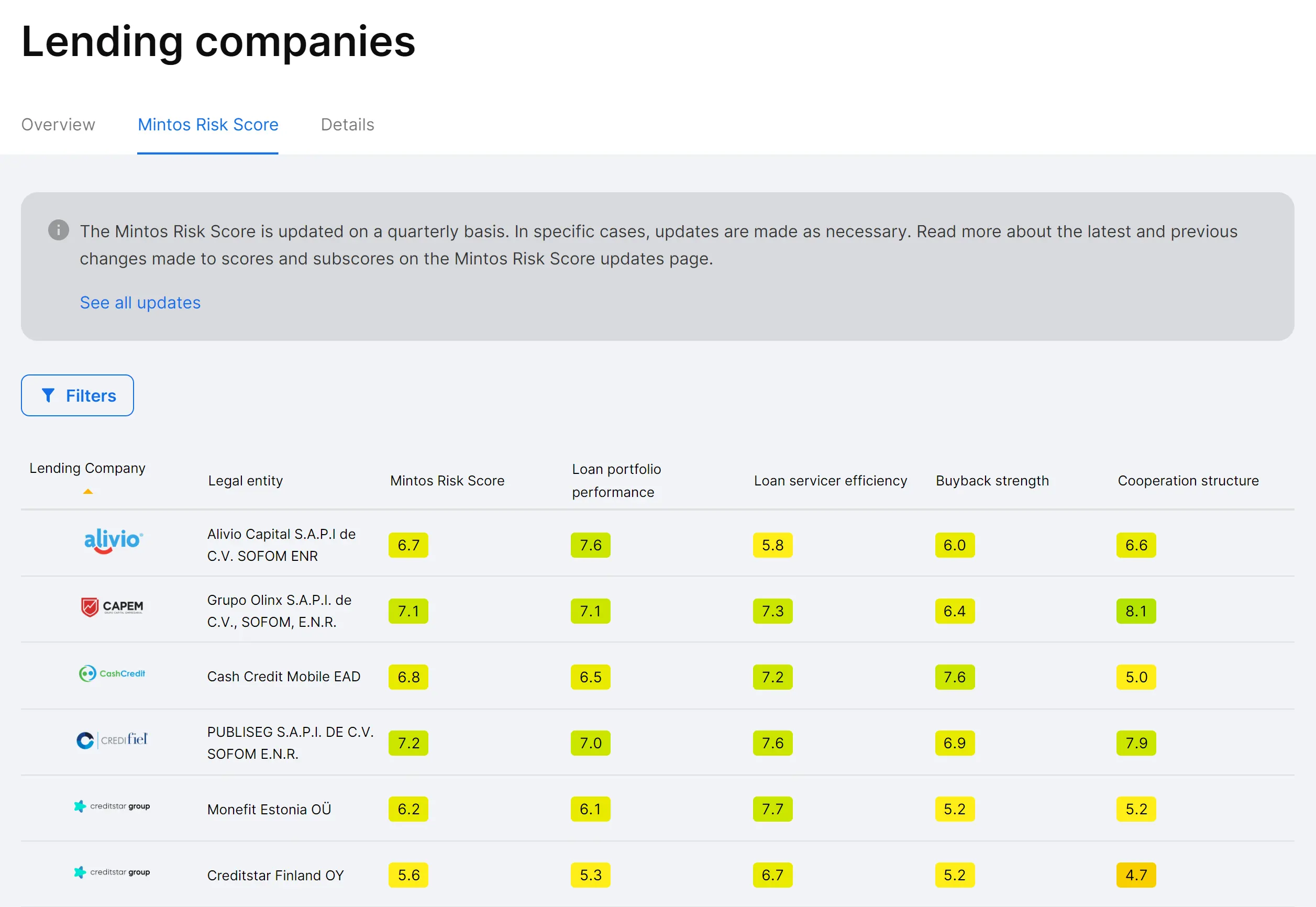

Mintos Risk Score

Mintos Risk Score is the platform's rating for individual loan originators. The rating is scoring criteria related to:

- Loan portfolio performance

- Loan servicer efficiency

- Buyback strength

- Cooperation structure

While Mintos’ risk scores can serve as a rough guide when building your portfolio, we don’t recommend relying on them too heavily. These scores can change quickly, often without investors noticing.

If you’re looking for a more reliable way to assess Mintos lenders, we suggest reviewing the loan originator section above. There, you’ll find a clear overview of key financial metrics from the largest loan originators on Mintos, including the debt-to-equity ratio and the equity-to-assets ratio over the past two years.

For investors planning to commit larger amounts, it’s essential to go one step further: review the financial reports of individual loan originators and carefully evaluate the country risk in which they operate.

Keep in mind that so-called “independent Mintos lender ratings” can be misleading. No external organization has access to the same level of data as Mintos itself, making Mintos the primary source of comprehensive lender information, although it is still not entirely free from conflicts of interest.

Under normal market conditions, investors on Mintos can expect average returns of around 9% per year when investing in broadly diversified loan portfolios. However, actual results can vary significantly.

For example, in 2020, the net return for so-called “well-diversified” portfolios dropped to just 2% as multiple risks materialized. This illustrates how quickly market events and loan performance can impact your earnings.

Ultimately, your portfolio’s return depends largely on two factors: the prevailing interest rates on available loans and the overall performance of the underlying loan book.

Correlation between Performance and Return

Let’s assume you invest €10,000 in a broadly diversified portfolio on Mintos with a 10% APY. Based on current performance levels of around 75%, you would earn approximately €750 in interest per year, while €2,500 of your capital could end up locked and unavailable.

As liquidity decreases, the risk of having funds locked in “recovery” grows significantly. After one year, your liquid portfolio would consist of about €7,500 in capital plus €750 in interest.

It’s important to note that funds in recovery typically do not accrue interest, which further reduces your overall return. On top of that, you have no guarantee of when—or even if—you will recover this money.

Investors can earn significantly more stable returns on other platforms. Are you wondering how Mintos compares to Esketit? Check out our comparison Esketit vs Mintos.

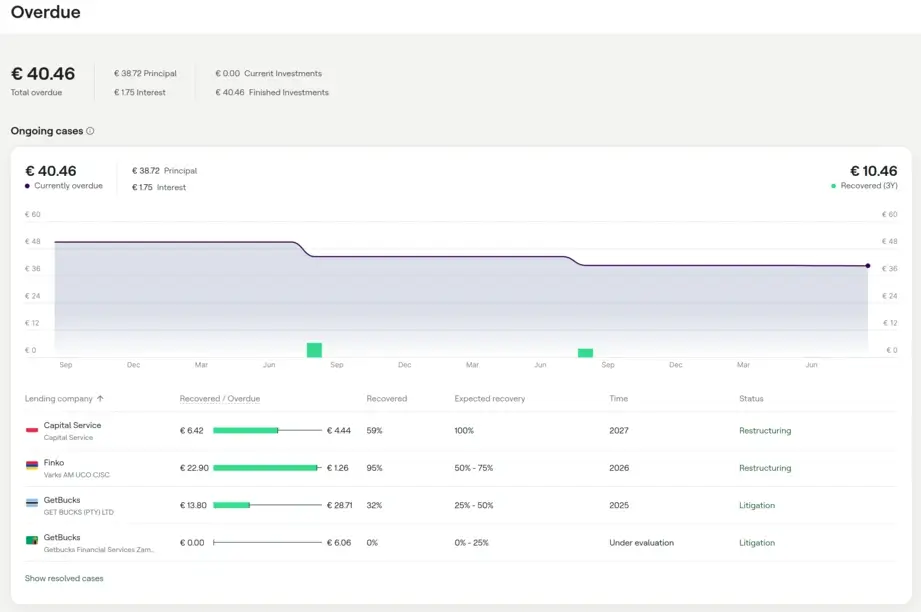

Mintos Recoveries

Mintos provides regular updates on the progress of loan recoveries, which we cover in detail in our monthly performance updates on our YouTube channel. If you’d like to track the status of your own overdue loans, you can do so by visiting mintos.com/en/overdue. Since Mintos doesn’t offer a straightforward navigation path to this page, you’ll need to enter the link directly into your browser.

When investing in Mintos, it is essential to familiarize yourself with the typical recovery process.

4 Stages of the Debt Recovery Process

- Monitoring - Mintos evaluates triggers such as breach of the law, equity to asset ratio, financial performance, unfavorable development in the market or negative changes in the management

- Limitation - Mintos limits the exposure of loans from the loan originator (placement of new loans is paused or suspended)

- Restructuring - Mintos negotiates a restructuring plan where the loan originator agrees to cover obligations toward investors

- Liquidation - Mintos takes legal action against the lender

If you decide to invest on Mintos, you should expect that some of your funds will eventually get stuck in "pending payments" or "in recovery", which limits your liquidity, increases the risk, and lowers your return.

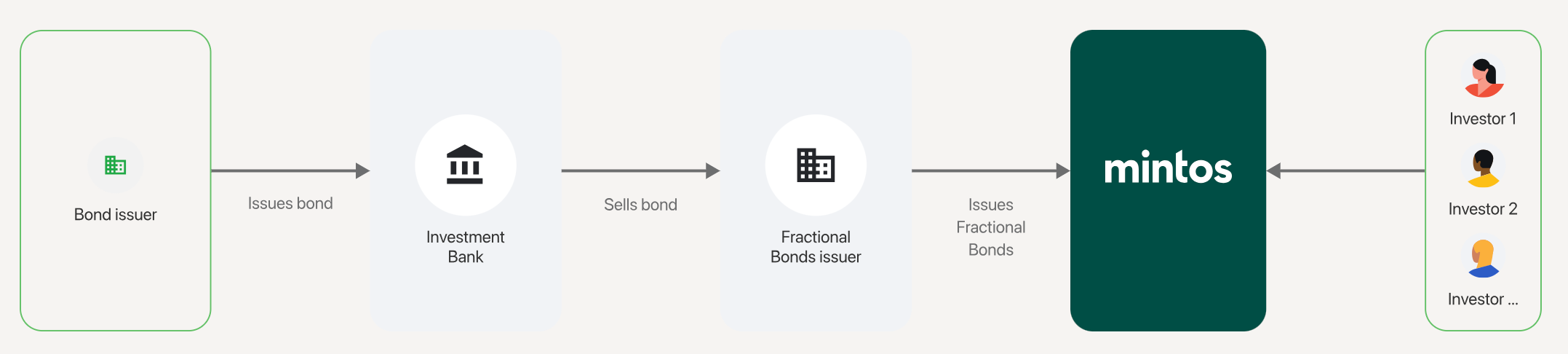

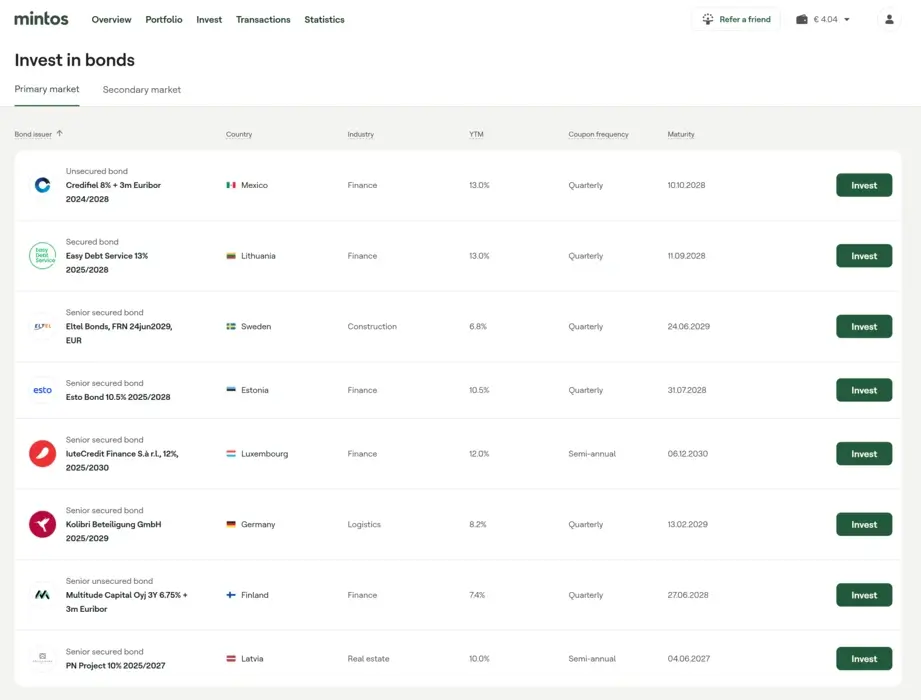

Mintos Bonds Review

Mintos is the only P2P lending marketplace offering the possibility to invest in fractional bonds for as little as €50. The platform has just started offering these investments, so the currently available bonds are somewhat limited.

Bonds on Mintos typically have longer loan terms, fixed yields, and quarterly interest payouts. All bonds can be sold on the secondary market, which may increase their liquidity. Every bond comes with a base prospectus, where you can learn more about the terms and conditions.

As Mintos informs its users when investing in fractional bonds, you don't invest directly in the bond but rather via a bond-backed security issued by a special-purpose vehicle within the Mintos group.

It's worth noting that investing in fractional bonds comes with similar risks to those associated with investing in loans.

Additionally, if you decide to sell your fractional bond on the secondary market, you might not be able to find a buyer who is willing to pay the initial price.

You can invest in bonds on Mintos by navigating to the menu item Invest -> Bonds.

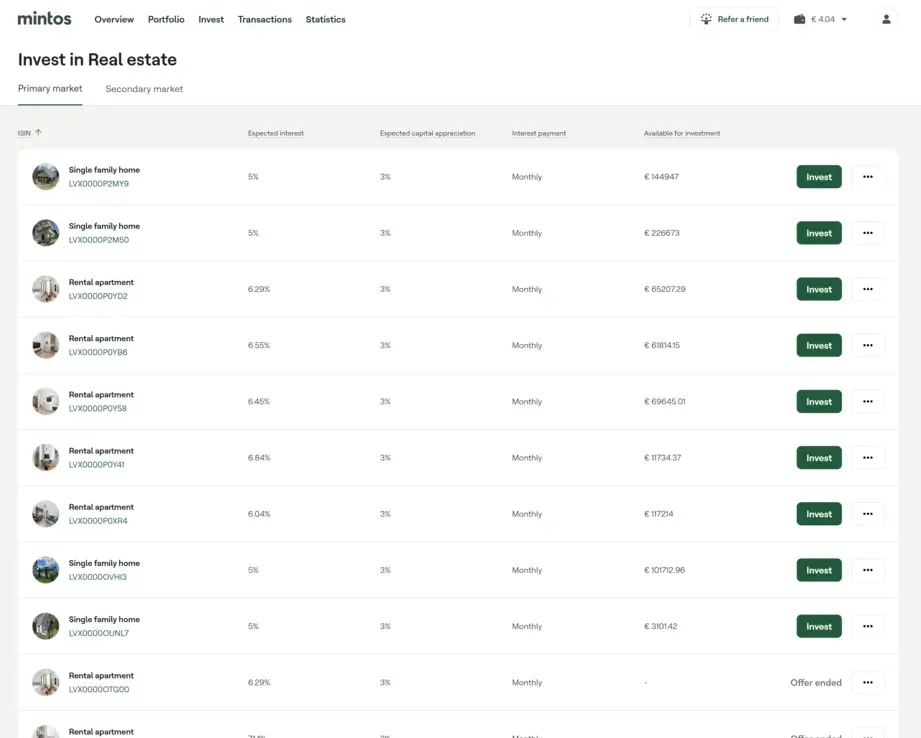

Mintos Real Estate Review

Mintos offers investments in residential real estate properties in cooperation with the Austrian fintech company Bambus.

Bambus Immobilien GmbH purchases properties from homeowners, who retain the right to live in the home while paying monthly rent. This system enables owners to utilize their equity for additional investments.

The rental properties on Mintos are offered via Notes, allowing you to start investing with as little as €50. The average interest (net rental income) is around 6%, with an expected annual capital appreciation of 3%.

This type of investment is backed by an underlying bond. The maturity of the real estate security is 10 to 25 years. Investors on Mintos have the option to sell their investments on the secondary market.

Investments in real estate rental properties carry significant risks, as outlined in the Key Information Sheet, which you can review for every property listed on Mintos.

You can invest in bonds on Mintos by navigating to the menu item Invest -> Real estate.

Mintos ETF Review

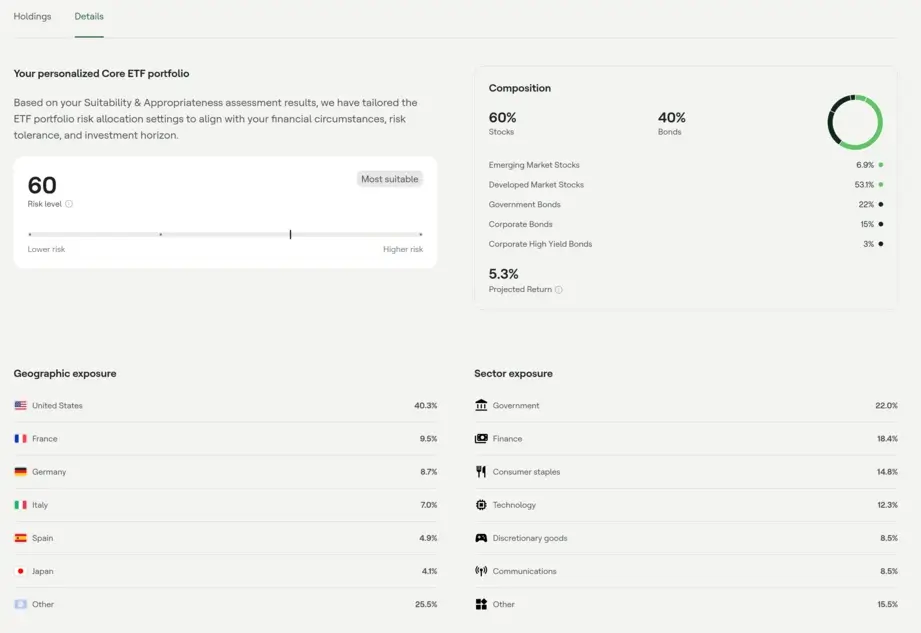

Mintos also offers investors the option to diversify beyond loans by investing in its Core ETF, which serves as a diversified portfolio of other ETFs.

While Mintos itself doesn’t charge management fees, you will still pay the Total Expense Ratio (TER) of the underlying fund, which is usually around 0.1% per year.

You can access the Core ETF through the platform by navigating to Invest → ETFs.

The allocation of your Core ETF portfolio is based on the results of the Suitability & Appropriateness assessment you complete when signing up on Mintos.

You can view the exact composition of your securities by selecting the Details tab in your account.

One of the main benefits of this product is accessibility; you can start investing with as little as €50. Mintos also handles automatic portfolio rebalancing for you.

By default, the Core ETF is structured with 60% in global equities, providing broad exposure to stock market growth, and 40% in European bonds, designed to offer more stable returns aligned with short- to medium-term market yields.

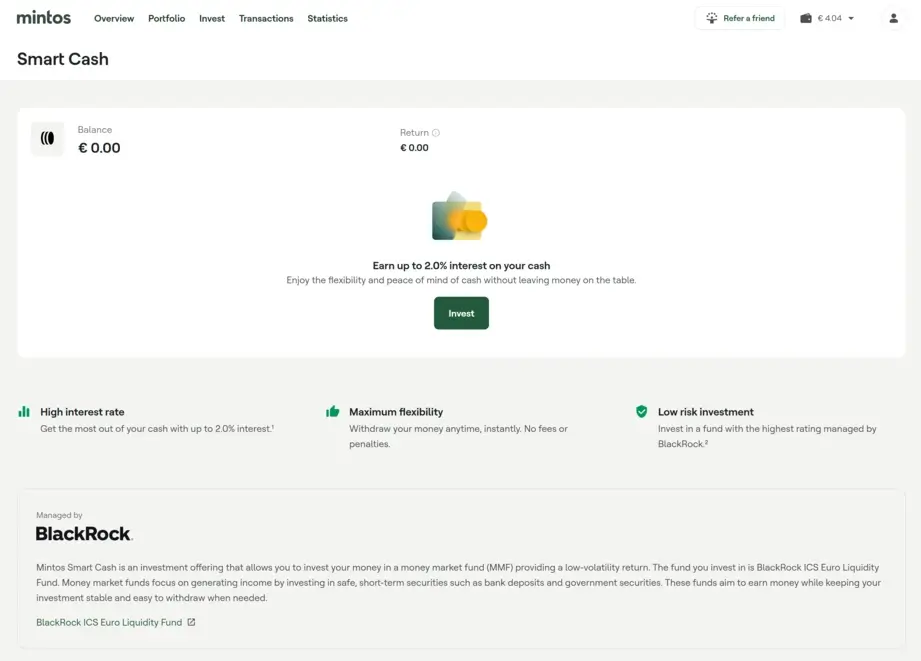

Mintos Smart Cash

Smart Cash is Mintos’ cash management product that invests your funds into a money market fund (MMF).

Money market funds are generally considered low-risk and highly liquid, aiming to provide steady income by allocating capital into short-term, secure instruments such as bank deposits and government securities.

This makes them attractive for investors who want stability and quick access to their money.

With Smart Cash, you benefit from:

- High interest rate – Earn up to 2.0% interest on your cash.

- Maximum flexibility – Withdraw your money anytime, instantly, without fees or penalties.

- Low risk profile – Invest in a fund with the highest rating, managed by BlackRock.

That said, Smart Cash and money market funds are not guaranteed investments. The value of your investment can fluctuate, and your capital is at risk.

When you invest in Smart Cash, your money is allocated to the BlackRock ICS Euro Liquidity Fund, a low-volatility net asset value (LVNAV) short-term MMF. This fund is issued by Institutional Cash Series plc, an investment company authorized and supervised by the Central Bank of Ireland.

You can turn on Smart Cash in your account by navigating to Invest -> Smart Cash.

Note that Mintos charges an annual fee of 0.19% on your balance with the Smart Cash product.

Mintos & Taxes

Another change investors are experiencing with Notes is the requirement to withhold taxes on their earnings.

As you receive interest from investments in Notes, Mintos will automatically withhold tax based on the applicable tax rate.

Tax rates on Mintos

- 20% for private investors and tax residents of Latvia

- 5% for private investors that are EU/EEA residents outside of Latvia (no documentation is required)

- 0% for Lithuanian tax residents (tax certificate is required); otherwise, 5%

- 20% for investors from outside of the EU/EEA (can be reduced if a tax certificate is provided)

- 0% for legal entities

When you report taxes in your country of tax residence, you may usually lower the taxes paid by the withheld amount, so your effective rate will be the same as if you invested in claims. Mintos provides tax reports and income statements in users' dashboards.

This is only valid if your country has a double tax treaty with Latvia.

If you don't want to deal with this hassle, you can also invest on Mintos as a company for which no taxes are deducted.

If you reside outside the EU or don't provide a tax residence certificate, Mintos will deduct 20% tax from your earnings.

Is Mintos Safe?

That's what we're going to address in this section.

Let's have a look at the safety of your investments on Mintos.

Who Runs the Company?

Mintos is run by its Co-founder and CEO Martins Sulte. Martins has been leading the company since its inception back in 2015. He also worked as a six-year financial analyst at the SEB investment bank.

Martins Valters co-founded the platform. He is currently Mintos's COO.

Both gentlemen gathered valuable experiences at Ernst & Young before launching their platform.

Watch our P2P talk with the CEO and co-founder of Mintos to get insights about the lessons learned from 2020, a critical period for Mintos.

Who is the Company’s Legal Owner?

Four angel investors and company shareholders fund Mintos.

Here is the list of the principal shareholders of Mintos:

- Maris Keiss (co-founder of 4finance and Mogo)

- Aigars Kesenfelds (co-founder of 4finance and Eleving Group former Mogo and owner of several loan originators)

- Kristaps Ozos (co-founder of 4finance and Eleving Group former Mogo

- Alberts Pole (co-founder of 4finance and Eleving Group former Mogo

- Martins Sulte - CEO Mintos (decision maker)

- Martins Valters - CFO / COO

- Employees through stock options

Note that Mogo was renamed to "Eleving Group" in mid-2021.

Are There Any Suspicious Terms and Conditions?

Mintos is changing its terms and conditions according to what suits the company. Breaches of old T&C are ignored, and the new terms are being updated.

The terms and conditions will mostly favor the company and protect its interests. As an investor, you accept that Mintos is not responsible for any losses you might suffer.

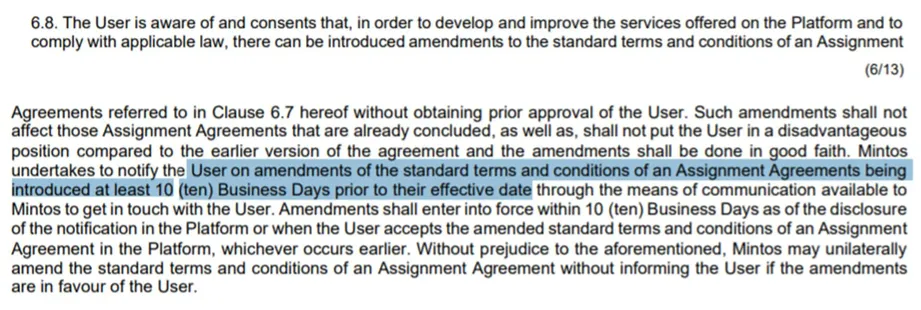

Old T&C Clause 6.8 - Amendments

Previously, Mintos could amend the terms and conditions of an assignment agreement without your approval.

Those amendments should not have affected already concluded agreements and should not put the user in a disadvantageous position compared to the earlier agreement version.

According to our understanding of the terms, Mintos didn't honor this clause as the P2P marketplace introduced loan extensions for already concluded agreements that put the users at a disadvantage.

It’s hard to imagine that any regulator would allow those practices in a regulated market.

We stopped monitoring Mintos' clauses as it no longer provides any substance for investors.

Past "updates" of terms and conditions show that clauses can be amended to fit the company's needs at any time, even if it puts the investors in a disadvantaged position.

If you are thinking about investing on Mintos, we suggest reading the current version of the terms and conditions before you invest.

Curious about other platforms? Head over to our ⚖️ P2P lending platform comparison for a quick overview of the currently available platforms.

Usability

Mintos is designed to be user-friendly, featuring an intuitive interface that makes navigation easy. You can quickly get an overview of your assets and track the performance of your multi-asset portfolio. By selecting individual assets, you can access more detailed information or choose to increase your investment.

We’ve already discussed how straightforward it is to invest in Real Estate, ETFs, Smart Cash, and Bonds. When it comes to loans, however, Mintos offers several different investment options. Let’s take a closer look at these in more detail.

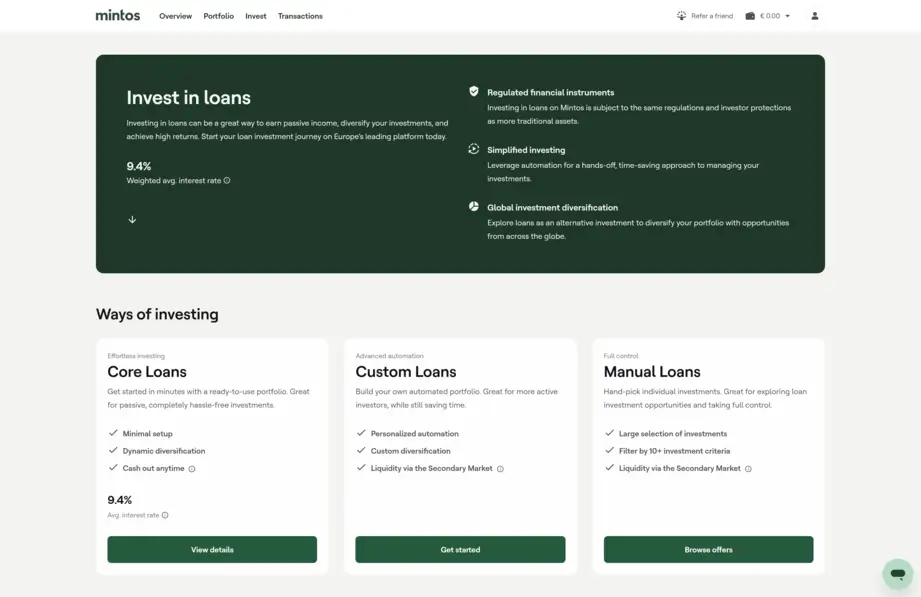

Mintos Core Loans

The Mintos Core Portfolio is the revamped version of Mintos’ previous products, including Mintos Strategies and Mintos Invest & Access.

It’s designed for investors who want a fully automated, diversified, and hands-off investment experience – while still targeting high returns.

Key Features:

- Weighted average interest rate: 9.4%

- Fully automated: No manual loan selection required

- Dynamic diversification: Your investment is spread across many loans

- Cash out anytime: Flexible liquidity

- Management fee: 0.39% annually (charged monthly)

Example: With a €1,000 portfolio, the monthly fee is approx. €0.32 or €3.90 per year

How It Works

Your "Core Loans" portfolio (formerly known as Mintos Core or Diversified Strategy) diversifies across all current loans with a Mintos Risk Score between 10.0 and 4.0, and includes only loans with a buyback obligation.

- The algorithm prioritizes both diversification and returns

- Exposure per lending company is capped at 15%, to reduce concentration risk

The portfolio invests only in Sets of Notes that have:

- Less than 20% exposure to late loans

- No loans that are more than 10 days overdue

- The investment criteria automatically adjust to market conditions for optimal protection and stability

Who It’s For

Mintos 'Core' Portfolio is ideal for investors looking for a simple, automated solution with high return potential, while maintaining a reasonable level of risk through algorithmic diversification. However, as with all P2P investments, underlying risks remain. Please note that Mintos may adjust the diversification settings periodically.

Mintos Custom Loans - Standard

If you want to get more control over your diversification, you can also create your own automated custom portfolio of loans and cherry-pick the lenders that fit your investment strategy.

You can use the custom strategy to either:

- Automate your investments based on your own criteria

- Invest manually based on your own criteria

The downside of this strategy is that you cannot exit your position immediately. If you wish to withdraw your funds prior to the end of the loan term, you will need to sell your investments on the secondary market.

Note that Mintos charges a 0.29% annual fee for the amount allocated to the Custom Strategy.

Automated or manual custom strategies should only be used by experienced investors. If you're starting with P2P lending, these options likely won't add much value.

Mintos Custom Loans - Advanced

The Mintos Auto Invest's functionality relies on the current market conditions. You shouldn’t just set it up once; you should also monitor supply and demand for investment opportunities and adjust your settings regularly.

Setting up your Mintos Auto Invest is a more advanced topic, so we have created a dedicated guide to help you learn how to create your own Mintos Auto Invest strategy.

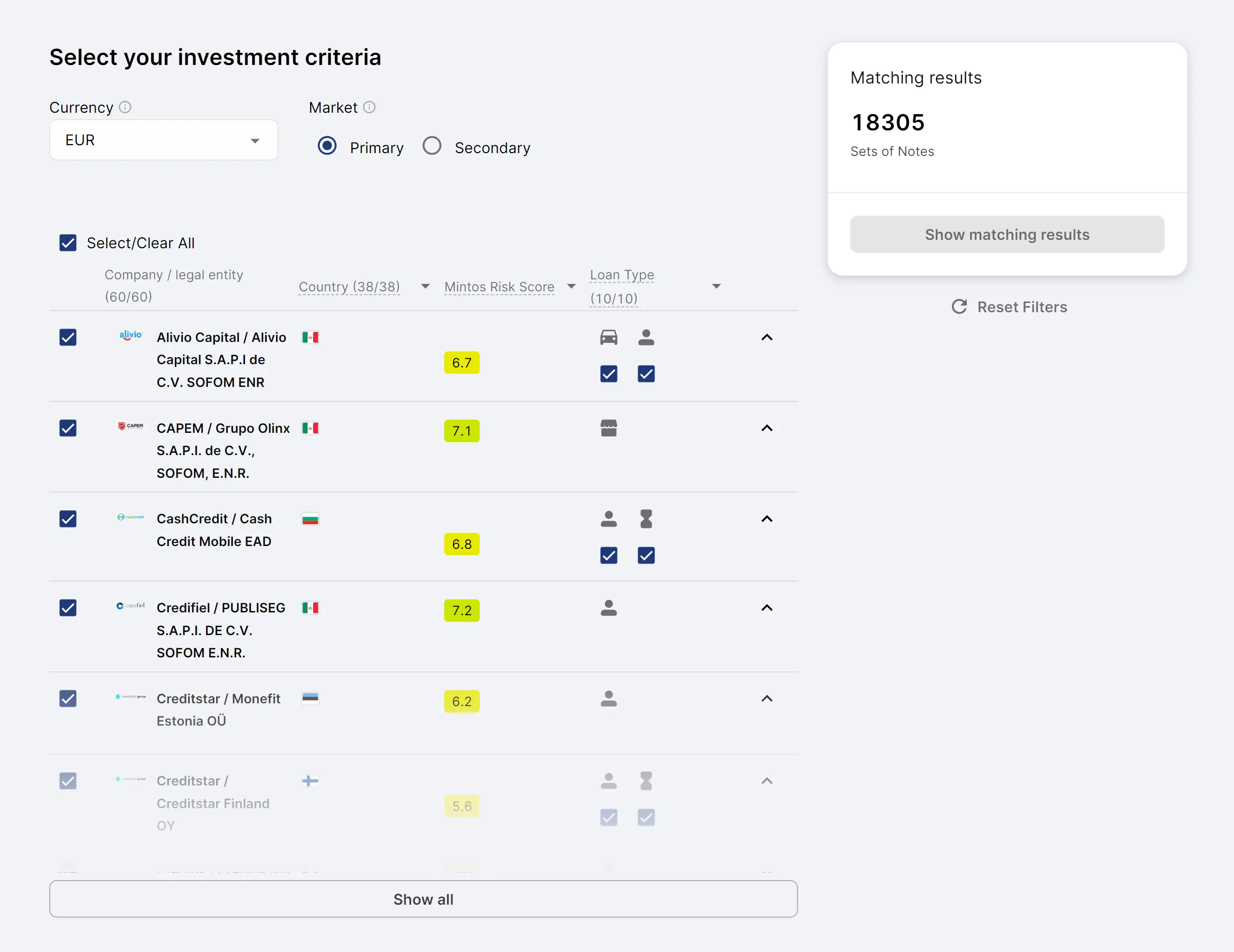

The automated custom strategy on Mintos enables you to take complete control over the diversification of your portfolio, which is particularly beneficial if you invest substantial sums of money.

Mintos allows you to define the following criteria:

- Currency

- Market

- Lending Company

- Country

- Risk Score

- Loan Type

- Buyback Obligation

- Loan Status

- Pending Payments

- Investment Structure

- Amortization Method

- Borrower APR

- Interest Rate

- Remaining Loan Term

- Maximum Portfolio Size

- Investment amount in one loan

- Diversification settings

As you can see, the Custom Automated Strategy offers numerous options.

After "fine-tuning" your settings, don't forget to click on "show matching results" to see how many loans match your criteria.

Accept the terms and save your settings if you are happy with the selection.

Remember that loan availability on Mintos fluctuates, and if your settings are too strict, you may experience cash drag (uninvested funds) because your settings won't match any available loans.

Liquidity

The speed at which you can withdraw your money depends on the product that you use, as well as the market conditions.

Selling on the Secondary Market

If you invest manually on Mintos or use the Custom Automated Strategy for long-term loans, you have the option to sell your investments on the secondary market. This can be useful if you want to access your funds before the loan reaches maturity.

Keep in mind that Mintos has reintroduced a 0.85% fee for selling investments on the secondary market. While we don’t usually trade there ourselves, it can be an effective way to improve liquidity if there are buyers available.

Liquidity on Mintos is generally good as long as the lender you’ve invested in is not suspended.

However, it also depends heavily on the type of asset. Short-term loans can often be sold quickly, whereas long-term real estate investments with 25 years remaining, or bonds with long maturities, may be far more difficult to exit.

Regarding withdrawals, Mintos processes requests within two business days, and in our experience, this feature has worked reliably without any issues.

Cash out with the Mintos Core Loans

If you choose to invest in Core Loans, you can usually withdraw your money at any time, provided enough other investors are using the same strategy to buy your shares.

However, this feature is highly dependent on overall market conditions.

If demand is low and no investors are actively using the strategy, you won’t be able to cash out, since there will be no buyers for your investments.

In such cases, you still have the option to sell your loans on the secondary market. But it’s important to note that if a lending company is suspended, you won’t be able to sell any part of its loan book, which could significantly limit your liquidity.

Support

If you’re new to P2P lending, you should start with a P2P platform that will answer your questions and educate you about P2P investments.

Some Mintos functionalities may require further explanation, and this platform features a customer support center to assist you with every step.

If you email Mintos’ customer support center, you can expect an answer within 48 hours.

Based on our personal experience, we recommend using the Live Chat function, which is significantly faster.

Notice

As Mintos frequently updates its terms and conditions, some of the information in this guide may be outdated. We suggest conducting your research before using any of the mentioned platforms to verify the accuracy of the information.

Mintos Alternatives

If you’re new to P2P lending, it’s best to start with a platform that not only provides investment opportunities but also helps you understand how P2P works.

Some of Mintos’ features may require additional explanation, and the platform offers a dedicated customer support center to guide you through each step. If you contact Mintos via email, you can typically expect a reply within 48 hours.

Based on our own experience, we recommend using the Live Chat option. It is significantly faster and more efficient than email, making it the best way to resolve questions in real-time.

Nectaro

If you are looking for a suitable Mintos alternative, Nectaro may be a good fit for you. The platform offers high-yielding loans from strong loan originators in Romania and Moldova.

While you won't be able to cash out immediately, the loan periods are relatively short, and the platform is very easy to use. If you want to learn more about this Latvian-regulated platform, please visit our Nectaro review.

Income Marketplace

The Income Marketplace may be a suitable option if you prefer using a single platform to diversify your investments.

This platform enables you to invest in various lenders from around the world. That way, you don't need to expose yourself to just one lender in one region, which may increase your risk.

Income Marketplace offers investments that pay up to 15% interest. Additionally, your money is protected by a buyback guarantee. Specific lenders even pledge their portfolios as collateral, increasing the safety of your investments.

Learn more about this platform in our Income Marketplace review.

Fintown

If you are looking for something different than Mintos, where you don't invest in payday loans in emerging markets, Fintown might be the right fit. This Czech platform offers interest rates of 10% and 12% on rental properties located in the city center of Prague.

So, instead of funding payday loans, you are funding rental units that generate rental income.

Learn more about how it works in our Fintown review.