Esketit Review Summary

Esketit is a P2P lending platform operating from Latvia, registered in Croatia since late 2025. It connects investors with loans from several loan originators, most of them owned by Esketit's founders. The average return is around 11% per year.

This Esketit review covers portfolio composition, liquidity risks, the Ireland-to-Croatia migration, and what the exit of Avafin and Money for Finance means for investors still on the platform.

Main Takeaways From Our Esketit Review

- 60-day buyback obligation on most loans — provided by founder-owned entities

- Avafin and Money for Finance have exited the platform

- Liquidity tools were suspended during the Ireland-to-Croatia migration

- Remaining loan originators have limited financial transparency

- Not regulated under the ECSP framework

Esketit has been operating since 2021 without a capital loss for investors. That track record matters. But the platform has changed significantly in the past 12 months, and those changes carry real consequences for investors.

Watch our latest Esketit video review here:

What Is Esketit?

Esketit (esketit.com) is a P2P lending platform founded by Matiss Ansviesulis and Davis Barons, the co-founders of the AvaFin Group, formerly known as CreamFinance, which was later sold to Capitec. The platform is registered in Croatia and operates from Riga, Latvia.

Investors can access business loans from Latvia, Spain, and Sri Lanka. Average annual returns sit at around 11%. The minimum investment is €10.

Pros

- Operational since 2021 — no investor capital losses to date

- 60-day buyback obligation on most loans

- Auto Invest feature available

- No fees for investors

- Income statements available for tax reporting

Cons

- Not regulated under MiFID II or the ECSP framework

- Avafin and Money for Finance have left the platform

- Liquidity tools suspended during the Croatia migration — no advance notice to investors

- Most remaining loan originators are founder-owned with limited financial disclosures

- Limited transparency from MDI Finance (Sri Lanka exposure)

Our Opinion

Esketit built a strong reputation between 2021 and 2024. Performance was consistent. The Auto Invest function worked well. The founders had credibility from their work at AvaFin.

The platform looks different now. Avafin was the strongest loan originator on Esketit — it offered regular financial disclosures and the best risk-return profile on the platform. It no longer lists loans. Money for Finance has also exited. These two departures shifted the portfolio composition significantly.

The remaining loan originators — Mojo Capital, Spanda Capital, MDI Finance, JMD Investments, and Credus Capital — are all either founder-owned or early-stage. Mojo Capital has limited public financial data. MDI Finance is a funding vehicle for a Sri Lankan lender, which we classify as a high-risk market. Spanda Capital is still establishing its track record in Spain.

The migration from Ireland to Croatia in late 2025 created an additional problem. Investors under the Irish entity lost access to the secondary market and the Auto Cash-Out feature. They received little warning. That episode revealed something important: liquidity on Esketit is operational, not contractual. Management can suspend it at any time.

We have been investing on Esketit since April 2022. Portfolio performance to date has been strong. But we are not adding capital at the current pace. The platform's risk profile has shifted, and the remaining loan book requires more scrutiny than it did 18 months ago.

You can review our current Esketit exposure on our P2P portfolio page.

Where This Platform Fits

Esketit suits investors who already hold a position and are monitoring it. For new investors, the current loan originator mix requires careful due diligence. The platform should not be treated as a core holding until liquidity tools are restored and the remaining loan originators provide more financial disclosure.

What Can Go Wrong

- Liquidity tools can be suspended without advance notice, as demonstrated in late 2025

- Investors under the Irish entity remain locked into long-term loans with no exit option

- Most loan originators are founder-owned — concentration risk is high

- MDI Finance operates in Sri Lanka, which we classify as a high-risk market

- A potential move to Latvia could trigger another liquidity freeze

- Mojo Capital and JMD Investments provide limited financial transparency

- Management is running multiple businesses simultaneously, which affects response times and platform focus

Esketit Bonus

P2P Empire readers qualify for a 0.5% cashback bonus. The bonus applies to all investments made within the first 90 days after registration. No promo code is required — signing up via our link is sufficient.

A loyalty bonus of up to +1% applies to investments above €25,000. This bonus is available only for loans from MDI Finance, Spanda Capital, and Mojo Capital.

Learn more on our Esketit promo code page.

Requirements

Esketit is open to investors aged 18 and above. Registration requires identity verification and a confirmed IBAN bank account.

- Be over 18 years old

- Pass the KYC process

- Verify your identity

- Verify your bank account (IBAN)

If you do not have a euro IBAN, a free N26 account or a Wise account are both compatible with the platform.

No suitability test is required. Onboarding is straightforward and typically completed within a few hours.

Risk & Return

Investing in P2P loans carries risk. You may lose part or all of your capital. Evaluate each loan originator separately before investing.

Buyback Obligation

Most loans on Esketit carry a 60-day buyback obligation. If a borrower is more than 60 days past due, the loan originator commits to repurchasing the loan from the investor.

The reliability of this commitment depends on the financial health of the loan originator. On Esketit, most loan originators with a buyback obligation are founder-owned entities. A financial failure at the originator level would make the buyback unenforceable.

| Loan Originator | Interest | Loan Type | Term |

|---|---|---|---|

| Credus Capital | 7% | Mortgage loan | 36 months |

| Mojo Capital | 12% | Business loan | 24 months |

| Spanda Capital | 10% | Defaulted debt (Spain) | 24 months |

| JMD Investments | 10% | Business loan | 12–24 months |

| MDI Finance | 12% | Business loan (Sri Lanka) | 12–24 months |

| Jet Finance | 10% | Car loan | 60 months |

Credus Capital, Mojo Capital, Spanda Capital, MDI Finance, and JMD Investments are all owned by Esketit's founders. This creates concentration risk. A problem at the founder level could affect multiple loan originators simultaneously.

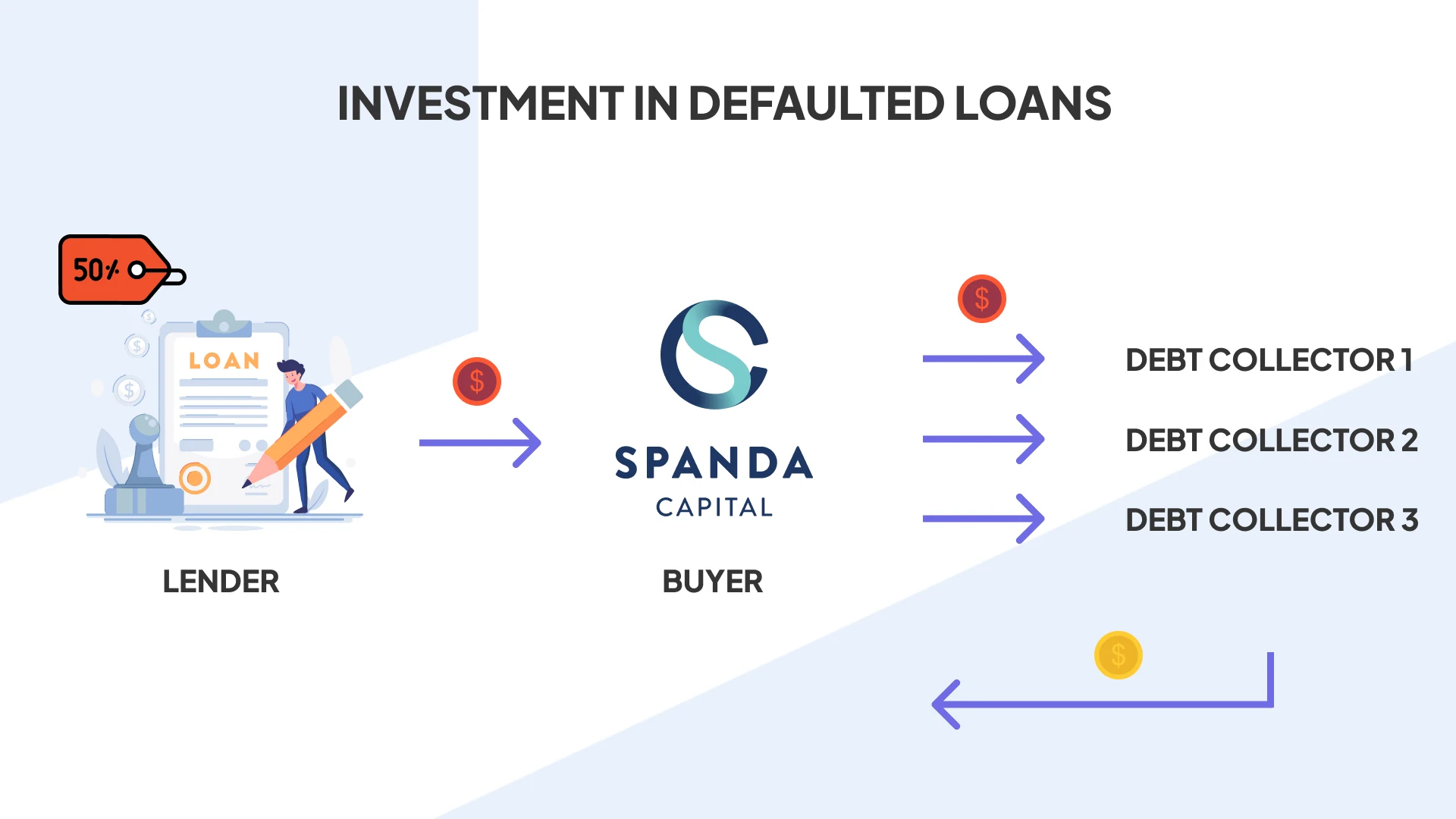

Spanda Capital — Defaulted Loans in Spain

Spanda Capital buys defaulted loan portfolios in Spain at a discount of 50%–60%. A debt collection agency recovers the portfolio. Spanda Capital takes a margin and pays investors 10%–12% per year on a 24-month loan term.

- Spanda Capital acquires a defaulted portfolio at a 50%–60% discount

- A third-party debt collection agency handles recovery

- Spanda Capital retains a margin from recovered amounts

- Investors receive principal and accrued interest at loan maturity

Recovery in Spain typically takes around two years. This aligns with the 24-month loan term. Spanda Capital is still early-stage. Track record data is limited. You can review its latest investor presentation for more detail.

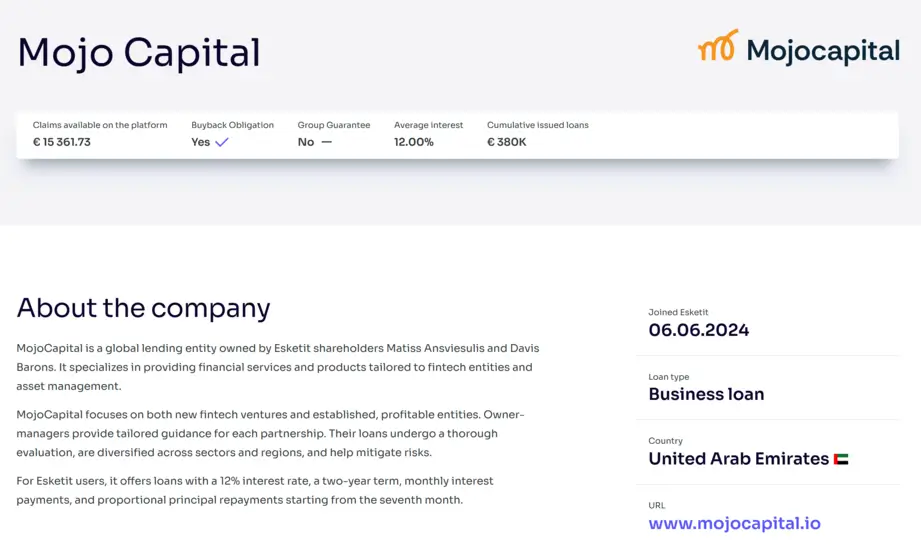

Mojo Capital — Fintech Business Loans

Mojo Capital provides business-to-business loans to fintech and asset management companies. It is owned by Esketit's founders Matiss Ansviesulis and Davis Barons.

Loans carry a 12% interest rate and a 24-month term. Principal repayments start from month seven. Monthly interest payments are made throughout.

Mojo Capital has limited public financial disclosure. Investors cannot independently verify portfolio performance or default rates at this stage.

MDI Finance — Sri Lanka Exposure

MDI Finance is the parent company of Loanme.lk, a digital lending platform in Sri Lanka. Its top management operates from Riga. Esketit's founders own MDI Finance.

Investors in MDI Finance loans are indirectly exposed to the Sri Lankan consumer lending market. We classify Sri Lanka as a high-risk lending market based on our country risk model. The current interest rate offered is 12% per year.

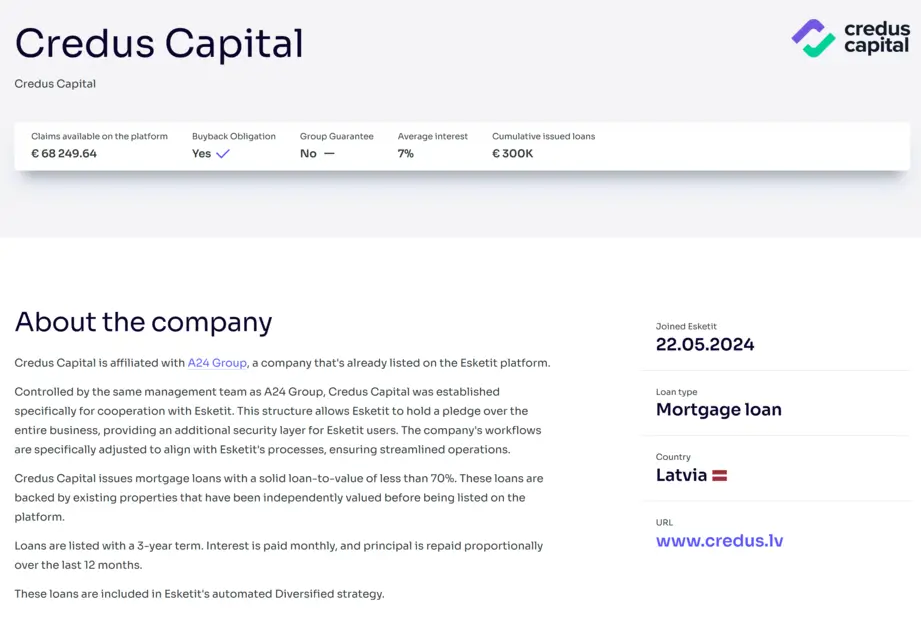

Credus Capital — Latvian Mortgage Loans

Credus Capital is an Esketit-owned vehicle that funds mortgage loans originated by Aksioma 24 in Latvia. Loan-to-value ratios range from 45% to 60%. Each loan is secured by a mortgage. Interest is paid monthly. The term is 36 months at a 7% annual rate.

Is Esketit Safe?

Esketit has operated since 2021 without any reported capital losses for investors. Below are the key factors to evaluate before investing.

Watch our Esketit safety and operations video here:

Who Owns the Platform?

Esketit is owned by Davis Barons and Matiss Ansviesulis. Both were co-founders of the AvaFin Group. They also own or control most of the loan originators listed on the platform.

This dual role — platform owner and loan originator — creates a structural conflict of interest. Investors should factor this in when assessing risk.

Who Runs the Platform?

Ieva Grigaļūne is the CEO of Esketit. She previously worked at Mintos. The founders remain involved in strategic decisions but also manage multiple other businesses, which has affected communication quality and platform responsiveness in recent months.

Storage of Funds

Investor funds are sent to a shared Esketit bank account. The platform does not provide individual IBAN accounts. According to the Terms & Conditions, investor funds are held separately from Esketit's operational funds. This is not independently audited.

Terms and Conditions — Key Clauses

Esketit reserves the right to amend its Terms and Conditions at any time. The platform notifies investors by email but does not specify a minimum notice period for accepting or rejecting changes. This is a weaker investor protection than regulated platforms typically offer.

The assignment agreement is available to registered users on the primary market. It is not accessible to non-registered users.

Usability

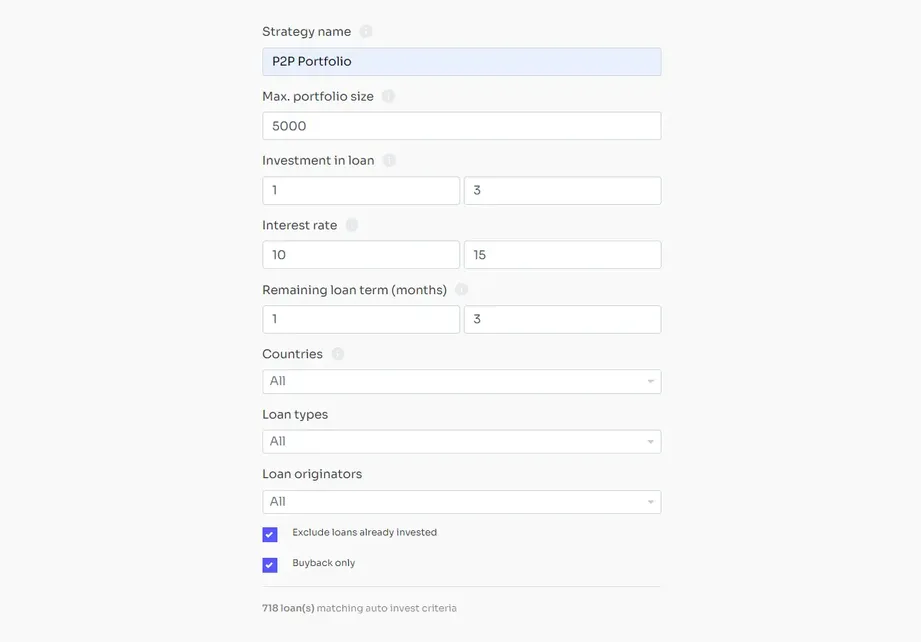

Esketit offers an Auto Invest feature for automated loan allocation. Investors can also invest manually through the primary or secondary market.

Auto Invest

The Auto Invest tool allows investors to filter by loan originator, interest rate, loan type, term, and country. Custom strategies require the secondary market for early exits. Only Esketit's pre-defined automated strategies offer the instant cash-out option.

Does Esketit Deduct Taxes?

Esketit does not withhold taxes on investment income. Investors can download income statements from their dashboard to submit to their local tax authority. For more information, see our guide on P2P lending taxes.

Liquidity & Secondary Market

Esketit offers a secondary market and two pre-defined automated strategies with an instant cash-out option. In practice, both tools have proven unreliable.

What Happened During the Croatia Migration

In late 2025, Esketit migrated its legal structure from Ireland to Croatia. During this process, the platform suspended the secondary market and Auto Cash-Out for all investors under the Irish entity. Investors had little warning before the tools were disabled.

Those investors remain locked into their existing loans with no exit option until maturity.

This is the most significant liquidity event in Esketit's history. It confirms that liquidity on the platform is operational — not contractual. Management can suspend it at any time, for any reason.

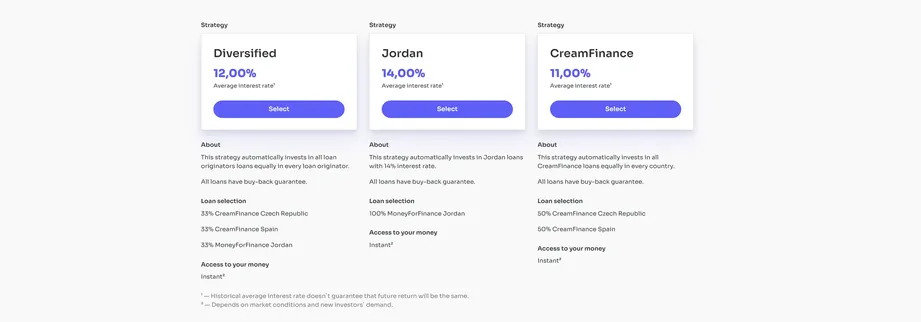

Automated Strategies & Instant Cash-Out

Esketit's pre-defined Diversified strategy includes an instant cash-out option. To activate it, navigate to the strategy, click "Edit," and select the "Cash-out" option. For the exit to work, other investors must be using the same strategy and absorbing your loan positions.

Custom Auto Invest strategies do not include this feature. Investors using custom strategies must use the secondary market to exit early.

The CreamFinance and Jordan automated strategies are no longer available. Avafin and Money for Finance have both exited the platform.

Secondary Market

The secondary market is available to investors who are not locked into the Irish entity. Loans can be listed with a discount to accelerate the sale. Premiums are also possible but may reduce the effective return below the nominal rate.

We have published a dedicated analysis of how premium pricing affects IRR on Esketit.

Support

Support quality has declined since the Croatia migration. Response times have increased, and several basic questions went unanswered or received delayed replies.

Before the migration, the CEO actively engaged in the official Telegram group, and responses typically arrived within one business day. That level of responsiveness has not been maintained in 2025 and 2026.

Founders managing multiple businesses simultaneously appear to be a contributing factor.

Esketit Alternatives

Investors looking for regulated platforms with stronger liquidity guarantees or more transparent loan originators may find the following alternatives more suitable.

Income Marketplace

Income Marketplace is an Estonian P2P platform with a buyback guarantee and a skin-in-the-game model, where loan originators pledge their loan books as additional security. Returns reach up to 15% per year. Read our full Income Marketplace review.

LANDE

LANDE is a regulated Latvian platform offering agricultural loans backed by grain, insurance, or other collateral. Average returns are 10%–11% per year. A secondary market is available. Read our LANDE review.

Fintown

Fintown is a Czech crowdfunding platform offering investments in short-term rental properties in Prague. Returns range from 10% to 12% per year, paid monthly from rental income. Read our Fintown review.