LANDE Review Summary

LANDE is a regulated Latvian crowdlending platform specializing in agricultural loans secured by land and machinery. Investors earn 11%–13% annually across Latvia, Lithuania, Romania, and Poland. The platform has issued over €30M in Latvian loans since 2019, with a cumulative default rate of 3.6%.

This LANDE review covers portfolio performance by market, default and recovery data, collateral quality, the new European Investment Fund guarantee, and key risks investors should factor in before allocating capital.

Main Takeaways From Our LANDE Review

- Regulated crowdfunding platform (ECSP license)

- Agricultural loans secured by land and machinery, average LTV of 44%

- Cumulative default rates: 3.6% (Latvia), 5.2% (Lithuania), 8.1% (Romania)

- European Investment Fund guarantee covers 80% of the principal on qualifying loans

- No loans written off to date; all defaulted loans remain in recovery

- Secondary market available for early exits

Watch our latest interview with LANDE CEO Nikita Goncars, covering five years of portfolio data and what to expect in 2026:

Ready to start earning interest on agricultural loans?

What Is LANDE?

LANDE Finance (formerly LendSecured) is a regulated crowdlending platform based in Latvia. It connects retail investors with agricultural borrowers across Latvia, Lithuania, Romania, and Poland.

Loans are secured by land, machinery, and grain buyer agreements. The minimum investment per loan is €50. Returns range from 11% to 13% per year, depending on borrower risk and market.

Pros

- ECSP-regulated crowdfunding platform

- Low average LTV of 44% across the loan book

- European Investment Fund guarantee on qualifying loans (80% of principal)

- Virtual IBAN accounts keep investor funds separated from platform accounts

- Secondary market available for early exits

- No cash drag and consistent loan availability across markets

- Latvian land loan default rate of 1.5% held through COVID and the Ukraine war

Cons

- Romania's cumulative default rate of 8.1% is the highest in the portfolio

- Recovery can take over three years on older defaulted loans

- No borrower-level debt visibility across multiple loans

- Loan extensions are not distinguishable from new loan applications in the platform UI

Watch our LANDE review to learn how the platform works:

Our Opinion

LANDE has been operating since 2019. It now manages a €22M portfolio across four markets, targeting €35M by year-end 2026.

The Latvian loan book is the benchmark. Over €30M has been issued, with a cumulative default rate of 3.6%. Land loans specifically carry a 1.5% default rate, a number that held through COVID, the Ukraine conflict, and the fertilizer price spike of 2022.

Romania is the weak point. The cumulative default rate stands at 8.1%, driven largely by the 2023 vintage when the team had limited local market knowledge.

LANDE has since tightened underwriting: the maximum machinery age has been cut from 10 to 7 years, a German valuation database has been integrated, and stricter local credit criteria have been applied. The 2025 vintage shows material improvement.

The European Investment Fund guarantee changes the risk profile for a portion of the book. Qualifying loans carry an 80% principal guarantee from EIF, an institutional backstop most platforms cannot offer. LANDE has secured €10M in guarantee capacity.

Two institutional banks now invest directly on the platform. Their presence adds an independent layer of credit assessment. LANDE did not change underwriting standards to achieve its 2026 growth targets; the volume increase is attributed to market maturity and new origination channels.

Borrower transparency remains a gap. There is no view of a borrower's total outstanding debt across multiple LANDE loans. Loan extensions are not distinguished from new applications in the platform UI. The CEO acknowledged both issues in our April 2026 interview, though no resolution timeline was given.

A new pooled investment product with daily liquidity is in development, targeting Q2 2026. It would allow fractional exposure across a large number of loans. The product is not yet live and is subject to regulatory approval. Execution risk is real: LANDE rebuilt its database in 2024 after problems with an earlier implementation.

Overall, LANDE is a credible, data-transparent platform in an underserved niche. The Latvian and Lithuanian books look solid. Romania carries more risk, and recovery timelines require patience.

Where This Platform Fits

LANDE suits investors who want secured, regulated exposure to agricultural lending with moderate diversification. It works best as a mid-weight portfolio holding for investors comfortable with illiquidity windows of 12 to 36 months on defaulted loans.

It is not suited to investors who need short-term liquidity or who cannot accept payment delays on a portion of their book.

What Can Go Wrong

- Recovery on older defaulted loans can exceed three years; capital is delayed, not necessarily lost

- Romanian loans carry an 8.1% historical default rate, and early vintage losses are still working through recovery

- No write-offs to date means investors cannot claim tax losses on delayed loans, which is particularly relevant for German tax residents

- Borrower debt concentration is not visible per project; a borrower can hold multiple active loans without this being flagged

- Approximately half of newly listed loans are extensions of existing borrowers, and these are not identifiable as such in the current UI

- Rapid portfolio growth targeting 2.5x year-on-year increases the risk of underwriting drift over time

LANDE Referral Code & Bonus

P2P Empire readers qualify for a 3% cashback bonus on investments made within the first 30 days after registration. No referral code is required; the bonus is applied automatically through our partner link.

Requirements

LANDE is open to investors from European Economic Area (EEA) countries with a SEPA bank account. Legal entities are not supported.

- Age 18 or older

- EEA citizenship and bank account

- KYC questionnaire and ID verification (passport or driving license)

Verification typically completes within 24 hours. Once approved, investors fund a virtual IBAN account operated by LemonWay. Funds are held at BNP Paribas and kept separate from LANDE's operating accounts. Transfers take one to three business days.

Risk & Return

LANDE operates in four markets. Each carries a different risk profile based on legal enforcement speed, market maturity, and loan product history.

In April 2026, we interviewed LANDE CEO Nikita Goncars to review five years of portfolio data. The interview covered default rates by market and vintage, recovery timelines, the EIF guarantee, and the 2026 growth plan. You can read the full summary in our LANDE CEO interview article.

Portfolio Performance by Market

Latvia

Latvia is LANDE's oldest and currently strongest market based on disclosed default data. The platform has issued over €30M in Latvian loans since inception, with approximately €1M currently in recovery.

- All-time default rate: 3.6% of total issued volume

- Land loan default rate: 1.5% (contributes 0.7pp to the overall figure)

- Main collateral: land and machinery

- Harvest and livestock loans discontinued after 2023

The weakest periods were 2022 and 2023, driven by financial loans, a product LANDE has since discontinued. Land loans have held up across multiple economic shocks.

Lithuania

Lithuania launched as LANDE's weakest market and has since become its strongest. A risk policy overhaul in 2023 significantly reduced delinquency. In 2025, the team identified only one loan more than 90 days past due.

- All-time default rate: 5.2%

- 2025 defaults: one loan

- Main collateral: land and machinery

Romania

Romania carries the highest cumulative default rate in the LANDE portfolio. Most historical defaults trace back to the 2023 launch vintage, when local market knowledge was limited.

- All-time default rate: 8.1%

- 2023 machinery loans: account for approximately 5% of the total defaulted book

- Recovery speed: slower than Latvia and Lithuania due to court processing times

- 2025 vintage: materially improved following underwriting changes

Changes since 2023 include a reduced maximum machinery age (from 10 to 7 years), integration of a German machinery valuation database, and tighter local credit criteria. Romanian loans carry the highest interest rates on the platform, which reflects the assessed risk.

Poland

Poland is LANDE's newest market. From launch, LANDE uses the notarial act structure (form 777), which allows direct enforcement via a bailiff without a court ruling. This is the strongest legal enforcement framework in the LANDE portfolio.

Loan conversion rates are lower than in Latvia at around 2%, partly due to broker-dominated distribution. Nikita expects Poland to outperform other markets in its first years based on the legal structure.

Loan Structure and Collateral

Loans range from €4,000 to €60,000 with terms of 4 to 36 months. The average LTV is 44%, with individual loans ranging from 13% to 58%.

Most loans are bullet structures: interest is paid monthly and principal is repaid at maturity once the harvest is sold to the grain buyer.

All collateral is assessed against the following factors:

- Borrower credit history, financial ratios, and tax compliance

- Planned and previous harvest volume and grain pricing

- LTV relative to independently appraised collateral value

- AML and KYC screening

LANDE receives 700 to 1,000 loan applications per month. Only 5% to 6% are accepted, and those undergo further evaluation before being listed on the platform.

Grain Buyer Agreements

For grain-backed loans, LANDE establishes a three-way agreement between the borrower, the grain buyer, and the platform. The quantity and price are agreed in advance, and the proceeds from the grain sale are used to repay the loan before the farmer receives the remainder.

LANDE only works with grain buyers who have a verified track record of over five years. 92% of crops are insured against weather events, including storms, hail, and heavy rainfall.

European Investment Fund Guarantee

LANDE has obtained a €10M portfolio guarantee from the European Investment Fund. Qualifying loans are covered up to 80% of the principal in the event of default.

This can materially reduce loss exposure on covered loans, assuming the guarantee applies and pays out as expected. Not all loans on the platform qualify. Investors should verify guarantee eligibility at the individual loan level.

Loan Extensions vs. Restructurings

These are distinct processes. Extensions are standard for agricultural lending. Farmers treat loans as revolving lines of credit, paying interest and partial principal before renewing at the end of each season. LANDE reassesses creditworthiness at each extension, reviewing financials, pledge quality, and performance.

Restructurings occur when a borrower is in financial difficulty. LANDE requests additional collateral and evaluates whether recovery prospects warrant continued investment.

- Approximately half of newly listed loans are extensions of existing borrowers

- There is no filter in the current UI to distinguish extensions from new borrower applications

- A borrower's total outstanding debt across multiple loans is not visible per project page

The CEO acknowledged both gaps in our April 2026 interview. No implementation timeline was given.

Default Recovery

LANDE has not written off any loans to date. Recovery continues until a bailiff confirms no remaining assets or income are available for collection.

- Fastest recovery: one day (borrower repaid after initial contact)

- Longest recovery: 3+ years (2023 loans still in progress)

- Real estate collateral: typically under 12 months without insolvency

- Machinery collateral: typically 6+ months to complete auction and transfer

- Romania: slowest recovery due to court processing times

- Poland: fastest expected recovery via notarial act enforcement

Interest continues to accrue at the original project rate throughout the recovery period. Capital may be delayed for years, and final recovery depends on the enforcement of collateral.

German tax residents should note that LANDE does not write off loans. Investors cannot claim tax losses on delayed capital until a final write-off is confirmed, and that has not yet occurred on any loan.

Why Borrowers Default

The primary driver is high indebtedness. Borrowers with thin equity cannot absorb seasonal shocks such as price drops, lower yields, or input cost spikes. LANDE targets borrowers with the highest equity levels relative to their loan size for this reason.

Secondary causes vary by product. Milk price volatility drove defaults in livestock lending, which is why LANDE exited that category. Poor grain seasons reduce margins but rarely cause default among well-capitalised borrowers.

Geopolitical and Macro Risks

Current fertilizer price volatility is significant but below the 2022 peak, when prices followed a tenfold increase in gas prices after Russia's invasion of Ukraine. Governments across LANDE's markets have introduced fuel tax rebates for farming, which partially offsets input costs.

On Mercosur: LANDE exited animal husbandry lending in 2024, the segment most directly exposed to Latin American competition. The direct impact on the current loan book is low. LANDE focuses on grain, which is less affected by Mercosur and more heavily supported by EU subsidy frameworks.

Returns

Latvian and Lithuanian loans typically offer 11%–12% annually. Romanian loans carry higher rates, reflecting the higher assessed risk. Most loans pay interest monthly with principal at maturity.

Cashback campaigns are offered periodically: 0.5% cashback on €500+, 1% on €1,000+, and 2% on €5,000+ invested in a single primary market transaction. These apply to larger single-loan deployments and partly offset cash flow disruptions from defaulted loans.

Is LANDE Safe?

Who Runs the Company?

LANDE is a brand of Secured Finance MGMT, owned by Ņikita Gončars and Edgars Tālums.

Nikita has received negative press coverage in Latvia in connection with a property restructuring business he ran prior to 2018. The company restructured high-interest payday loans secured on residential property. According to Nikita, 90% of cases were resolved and compensation was paid where clients could not repurchase their homes. The service was discontinued in 2018 and is not planned for the future. He described the media coverage as the result of competitor-driven pressure.

We visited LANDE's office in Riga and discussed this topic directly with the CEO. His account was consistent and detailed.

Regulatory Status

LANDE holds a regulated crowdfunding service provider (CSP) license under the ECSP framework. This is the same regulatory standard applied to other regulated Baltic P2P platforms.

Fund Storage

Investor funds are held in virtual IBAN accounts at BNP Paribas, operated through the payment institution LemonWay. Funds are legally separated from LANDE's operating accounts.

Terms and Conditions

LANDE does not specify a minimum advance notice period for T&C changes. An automatic email is sent when terms are updated. Loan agreements are generated automatically upon investment and are visible in the portfolio section.

We found no anomalies in the legal documents reviewed during our onboarding. Review the current version before investing, as terms may change.

Usability

Manual Invest

Investors can browse and select individual loans on the primary market. Each project page shows the loan amount, term, interest rate, borrower background, and collateral details. Appraisal reports for land-backed loans are available but not translated into English.

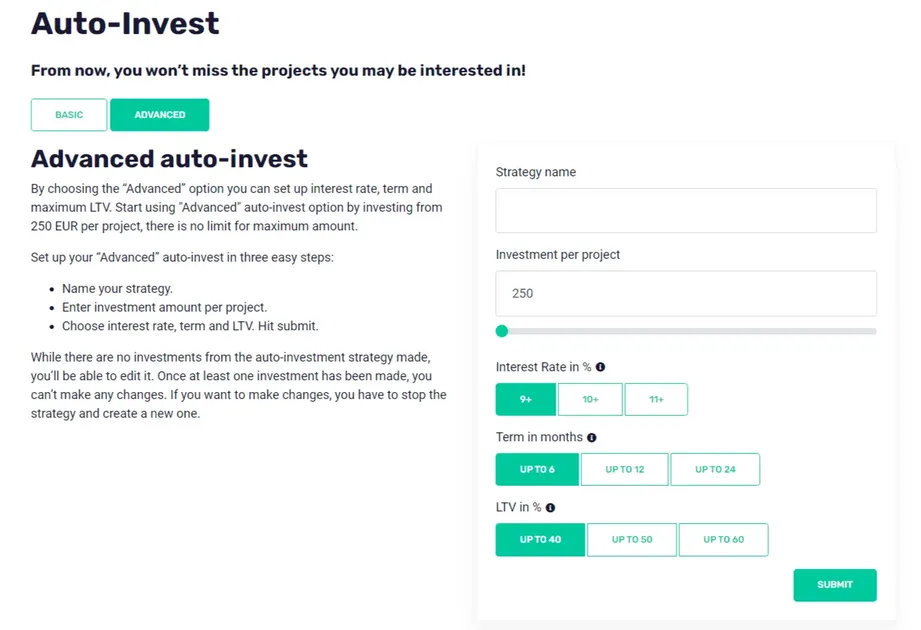

Auto Invest

LANDE offers a basic and advanced Auto Invest. The advanced version allows filtering by interest rate, loan term, LTV, collateral type, country, and payment schedule. The minimum per loan through Auto Invest is €100.

New investors should manually review a few loans before enabling Auto Invest to understand what collateral types and borrower profiles are available.

Does LANDE Deduct Taxes?

LANDE does not withhold Latvian tax on investor returns. Income statements are available for download under the "Balance" section of the dashboard. Submit these to your local tax authority as required by your country of residence.

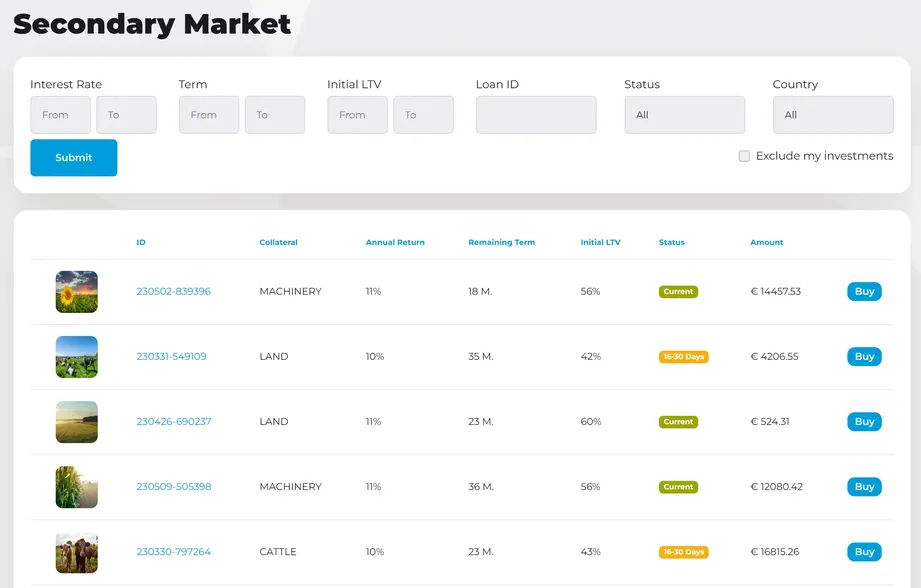

Liquidity & Secondary Market

LANDE offers a secondary market for early exits. Investors can list and purchase loans based on their own criteria.

- Loans under €100 in value must be sold in full

- Partial purchases of €50+ are available for loans above €100

- Only current loans with no delays can be listed for resale

- Defaulted loans cannot be sold on the secondary market

- Full bullet loans cannot be sold before the principal repayment date

- Loans cannot be listed during the funding phase

- No fees are charged for secondary market transactions as of April 2026

A new pooled investment product with daily liquidity is under development, targeting Q2 2026. It would provide fractional exposure across a large number of loans with a daily exit option. This product is not yet live and is subject to regulatory approval. We will update this section when it launches.

Support

We have been in contact with LANDE since its launch and visited the team in Riga in 2022. In April 2026, we conducted a further interview with the CEO covering portfolio performance and the 2026 growth plan.

Response quality at the management level has been consistently detailed. General inquiries can be directed to info@lande.finance.

LANDE Alternatives

Investors seeking different collateral types, markets, or risk profiles may consider the following alternatives.

Indemo

Indemo is a regulated Latvian platform investing in discounted Spanish mortgage-backed loans. The target return is above 15% annually, with capital and interest typically received after a two-year recovery process. See our full Indemo review for details.

Crowdpear

Crowdpear is a regulated Lithuanian platform offering real estate loans in Vilnius. It is one of the stronger-performing platforms in the regulated Baltic segment, with no reported payment delays. Read more in our Crowdpear review.

Nectaro

Nectaro is a regulated Latvian P2P platform offering consumer and business loans from Moldova, Romania, and the Philippines. Yields range from 12% to 13.5% per year. There is no secondary market, but most loans are short-term and repaid within roughly one year. More detail is available in our Nectaro review.