Afranga Review Summary

Afranga is a regulated Bulgarian P2P lending platform offering 8% to 16% per year on business loans from Stikcredit and several other Bulgarian lenders. Loans are secured by company assets under a direct loan structure. The platform relaunched under the ECSP framework in March 2025.

This Afranga review covers the lending structure, loan originator quality, regulatory status, liquidity, and the key risks investors need to understand before committing capital.

Main takeaways from our Afranga review:

- Regulated platform under the Bulgarian Financial Supervision Commission

- Direct loan structure with individual Lemonway accounts for investors

- 8%–16% per year with monthly interest and principal repayments

- Concentrated exposure to Bulgarian consumer lenders, with Stikcredit as the main originator

The following video offers an introduction to Afranga. Note that it was recorded before the platform received its crowdfunding license. For current information, read the sections below.

Pros

- Regulated under the ECSP framework

- Direct loan structure with clear legal claim against the originator

- Individual Lemonway accounts — investor funds segregated from the platform

- Above-average interest rates on medium-term loans

- Responsive support and transparent lender disclosures

Cons

- Heavy concentration in Bulgarian consumer lending

- Stikcredit default rate of 12%–15% of the loan book

- No auto-invest or secondary market at present

- Limited diversification across originators and geographies

Our Opinion of Afranga

Afranga is a smaller P2P platform that has grown up as the funding channel for Stikcredit — a Bulgarian consumer lender active since 2013. That origin still defines the platform. Most of the loan volume comes from Stikcredit, and the rest from a small number of additional Bulgarian lenders.

The March 2025 relaunch was a meaningful step up. Afranga now operates under the ECSP framework, uses a direct loan structure, and holds investor funds in individual Lemonway accounts. Legally and operationally, investors are in a much stronger position than under the old model.

The technical side is still catching up. A proper auto-invest and the secondary market are not live yet. Both were available on the old platform and are expected to return, but no firm timeline has been confirmed.

On credit quality, the picture is mixed. Stikcredit's impairments rose from €3.63M in 2023 to €5.07M in 2024 — faster than revenue growth. Management reports a default rate of 12%–15% of the loan book, which is high for established lenders. The loans have always carried real credit risk; that risk is now more visible.

Strategically, Afranga wants to become a pan-European marketplace for business loans. The platform has already onboarded Lev Credit, Credirect, Lendivo, and Swiss Funds. More lenders mean more diversification on paper, but also more originators to monitor — and less oversight than Afranga has over Stikcredit.

The main appeal remains the rate. Returns of 11%–16% are higher than those offered by most regulated platforms. That premium exists for a reason - to provide quick funding for Stikcredit to grow its loan book.

You can see our position on Afranga in our P2P portfolio.

Where This Platform Fits

Afranga is suitable as a satellite position — not a core holding. We recommend limiting exposure to 10%–15% of a diversified P2P portfolio. Two factors drive that cap: the heavy concentration in Bulgarian consumer lending, and the elevated credit risk reflected in Stikcredit's rising impairments and 12%–15% default rate. The platform works best for investors who want above-average yields from a regulated platform and are comfortable sizing the position accordingly.

What Can Go Wrong

- Stikcredit's default rate sits at 12%–15% and impairments are growing faster than revenue — further deterioration would directly affect investor returns

- Most of the loan book is concentrated in Bulgarian consumer lending — a local regulatory or economic shock would hit the entire portfolio

- No secondary market is available at the moment — capital is locked until the loan matures

- No auto-invest means investors must build positions manually

- As Afranga onboards more third-party lenders, the platform will have less oversight than it does over Stikcredit — investors need to evaluate each new originator independently

- Above-average interest rates are not guaranteed to last — rates may compress as the platform scales

Afranga Promo Code

Readers who sign up through our partner link receive a 0.5% cashback bonus on all investments made within the first 90 days after registration. No special Afranga referral code is needed.

Requirements

To invest on Afranga, investors must meet the following requirements.

- Be at least 18 years old

- Hold citizenship in an EU/EEA country

- Have a bank account in an EU/EEA country

- Reside in a country with equivalent AML/CFT standards

- Complete the platform verification process

Afranga lists loans in EUR. Deposits should be made from a EUR account to avoid currency exchange fees.

Risk and Return

Afranga launched in early 2021 and operated without formal supervision until March 2025. It has since relaunched as a regulated platform under the ECSP framework, offering business loans issued by Bulgarian lenders.

Loan durations range from 6 to 36 months with interest rates between 11% and 16%. Monthly repayments cover both interest and principal. Stikcredit AD is licensed and regulated by the Bulgarian National Bank, while Afranga falls under the Bulgarian Financial Supervision Commission.

Beyond Stikcredit, Afranga lists loans from Lev Credit, Credirect, and Lendivo. The platform also offers lower-yield investments in the loan book of Swiss Funds, a Czech-based lender. Financial metrics for each lender are available in the Loan Originator section.

Secured by Company Assets

Business loans on Afranga use a direct loan structure rather than the SPV-intermediary model used by some other platforms. This produces clearer documentation, a direct legal claim against the originator, and easier recovery in the event of default. Both individual and collective legal action are possible if needed.

The regulated framework strengthens investor protection further. Borrowers are now fully liable for the loan with all company assets. This replaces the old structure, where investors held fragmented claims across individual loans — making exposure and recovery harder to assess.

As of year-end 2024, Stikcredit reported total assets of €28.3M. In our conversation with the CEO, management emphasized that Stikcredit has consistently honored its obligations without payment delays.

Stikcredit Loan Book Performance

Net impairment costs on loans and receivables totaled €3.63M in 2023, down from €4.66M in 2022. In 2024, impairments rose again to €5.07M. Part of that reflects loan book growth, but it also points to a rising share of non-performing loans.

According to the CEO of Afranga, Stikcredit's default rate sits at 12%–15% of the loan book. That is elevated even for the short-term consumer lending segment and warrants close monitoring as the portfolio grows.

You can learn more about the CEO and the platform's direction in the interview below.

Is Afranga Safe?

Who Leads the Team?

Afranga is led by Svetlin Sabev, who co-founded the platform in 2021 and now serves as its sole shareholder. With eight years of experience in lending, Sabev launched Afranga to create a reliable funding channel for Stikcredit.

The platform is supported by a professional team, though individual profiles are not currently listed on the About Us page. We have flagged this point with the CEO.

Who Owns the Platform?

Afranga was founded in December 2020 and originally owned by Stefan Topuzakov, Kristian Kostadinov, and Svetlin Sabev. In 2023, Sabev acquired 100% of the company and has been the sole owner since.

Discover more about the CEO and the platform's future plans.

Usability

The interface is clean and easy to navigate. Essential information is accessible quickly, and the platform is noticeably simpler to use than IUVO, an unregulated Bulgarian marketplace.

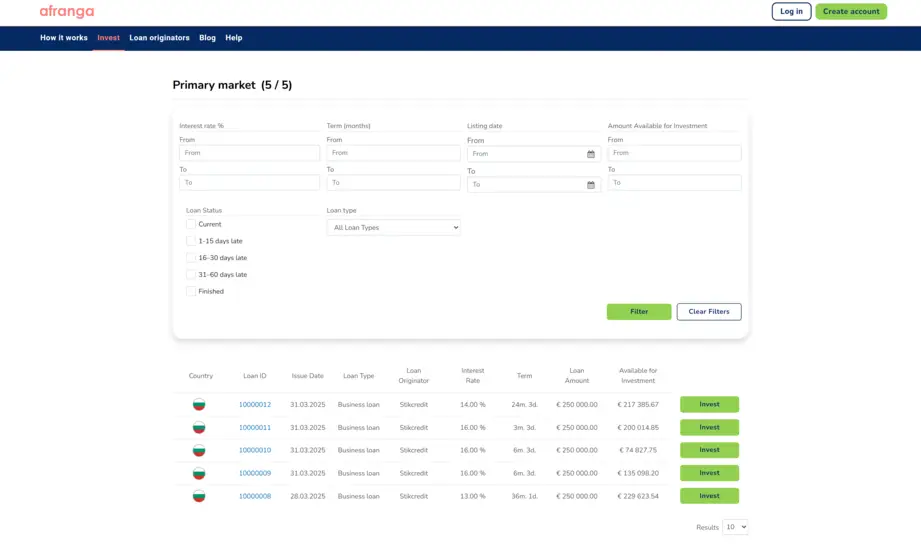

Primary Market

The relaunched platform currently offers only manual investing via the primary market. Auto-invest is expected to return at some point, according to the CEO.

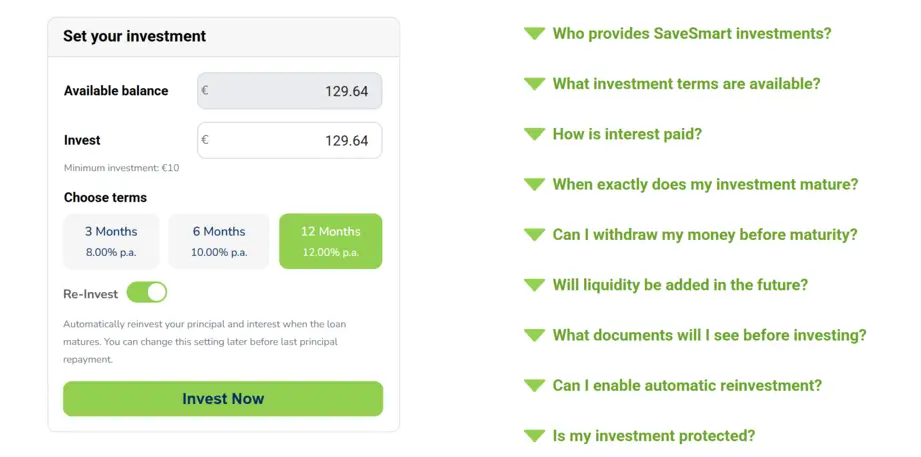

Afranga SaveSmart

SaveSmart is a fixed-term investment product with three options: 3 months at 8%, 6 months at 10%, and 12 months at 12%. Interest is paid monthly and principal is returned at maturity. Automatic reinvestment into a new term can be enabled.

SaveSmart is not a savings account or bank deposit. Structurally, investors provide a private loan to the originator (currently Stikcredit), facilitated by Afranga. Capital is exposed to loan-originator risk and is not covered by any deposit guarantee scheme.

There is no liquidity option at launch — investments cannot be withdrawn early, and maturity may extend by up to one additional calendar month. Afranga has stated that liquidity features may be introduced later, but no timeline is confirmed.

Investments fall under the ECSP framework. Investors receive standard documentation, including the KIIS and loan agreement, before investing.

🧾 Does Afranga deduct taxes?

Under Bulgarian law, the withholding tax on interest is 10%. If you earn €100 in interest, Afranga withholds €10 and reports it to the national revenue agency. A tax statement is available for annual filings.

Liquidity

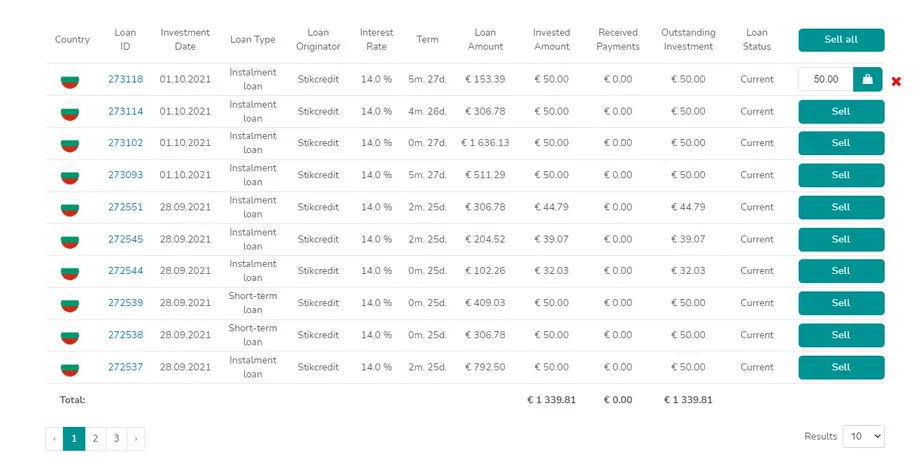

Afranga previously offered a secondary market allowing investors to sell loans. The feature is not yet available on the relaunched platform.

On the old version, listing worked as follows: navigate to My Investments, select the loans to sell, and confirm. From a secondary-market perspective, a premium or discount could be applied. Sale time depended on loan size and demand — some users reported sales within a day. Accrued interest was only received once the loan was fully repaid.

Currently, the secondary market is not available. Investors should plan for capital to be locked until each loan matures.

Support

Afranga's support is responsive. Questions are typically answered within 24 hours, and the team does not hesitate to share details that are not publicly available on the website. You can reach out during business hours at support@afranga.com.

Afranga Alternatives

Afranga offers competitive interest rates, but investors looking for broader geographic and originator diversification or faster liquidity may want to consider the following platforms.

Income Marketplace

Income Marketplace is an Estonian platform with lending partners across Europe, Asia, and the Americas. All loans come with a buyback guarantee, and many originators also pledge their loan books as additional security. Returns run up to 15% per year. Learn more in our Income Marketplace review.

LANDE

LANDE is a Latvian platform focused on agricultural loans secured by grain, insurance, and other collateral. The platform is known for transparency and a strong track record of capital protection. Learn more in our LANDE review.

Nectaro

Nectaro is a regulated Latvian platform offering investments sourced from EcoFinance in Romania, Moldova, and the Philippines. Yields run up to 14,5% per year with regular cashback offers. Learn more in our Nectaro review.