Debitum Review Summary

Debitum is a regulated Latvian investment platform offering exposure to SME-backed securities. The platform has grown assets under management quickly, but the current portfolio appears far less diversified than it may seem at first glance.

Main takeaways from our Debitum review:

- Regulated platform with easy-to-use interface

- Not suitable for conservative investors

- High concentration and correlation risk

Read our Debitum review to learn more.

What is Debitum?

Debitum is a regulated Latvian platform offering investments in asset-backed securities from just €10. Investors on Debitum can earn up to 15% per year.

Pros

- Intuitive investment platform

- Regulated in Latvia

Cons

- No secondary market

- High concentration in one interconnected regional ecosystem

- Significant exposure to forestry, land, and construction-related businesses

- Platform history remains controversial

Disclaimer

We are not affiliated with Debitum or any of its previous legal entities. This overview highlights key aspects of the platform’s development and current structure.

Investors should verify the information presented, as we do not continuously monitor the platform. As a result, we have removed the rating.

Nothing on this page should be considered investment advice. For transparency, we have included additional feedback from management where relevant.

Our Opinion of Debitum

Debitum is not suitable for conservative investors. Based on the available data in 2026, the platform primarily finances a Valmiera-centric forestry, land, and construction ecosystem, with capital distributed across multiple issuers that appear operationally and structurally connected.

While this model has enabled fast growth in assets under management, it also creates concentration and correlation risk that investors should take seriously. Debitum may look like a diversified marketplace on the surface, but the underlying exposure appears much narrower than the number of issuers suggests.

Investors should therefore focus less on the number of listed issuers and more on the underlying economic exposure, ownership links, creditor relationships, and refinancing dynamics behind them.

Debitum 2.0 - What You Need To Know

Debitum 2.0 follows a different concept from its earlier version. The new management grew assets under management to around €60M, which is notable in a market where many platforms have struggled to expand due to limited high-quality loan supply. On the surface, Debitum appears to be growing while offering investors returns of up to 15% per year.

As of January 2026, Debitum reported the following portfolio allocation (Source: platform statistics):

- Evergreen Capital (€0.6M) - external lender

- Triple Dragon (€6.38M) - external lender

- Sandbox Funding (€10.32M)

- DN Funding Alpha - Ukraine-restructured loans (platform statistics: €0.2M / our estimate: €1.75M)

- Foresto (€25K)

- Juno Finance (€365K)

- Latvian Forest Development Fund (€33.65M)

- Baltic Terra (no statistical updates)

Based on this data, only a relatively small share of the portfolio appears linked to clearly external lenders, while most of the exposure is concentrated in a cluster of connected companies operating mainly in the Latvian forestry, land, and construction sectors.

Why This Matters

Debitum is often perceived as a marketplace with multiple independent originators. However, the majority of current outstanding exposure appears to be linked to companies operating in the same region, in related sectors, and, in some cases, with overlapping ownership, management, or creditor relationships.

That does not automatically mean wrongdoing. It does mean investors should be careful not to mistake issuer count for true diversification.

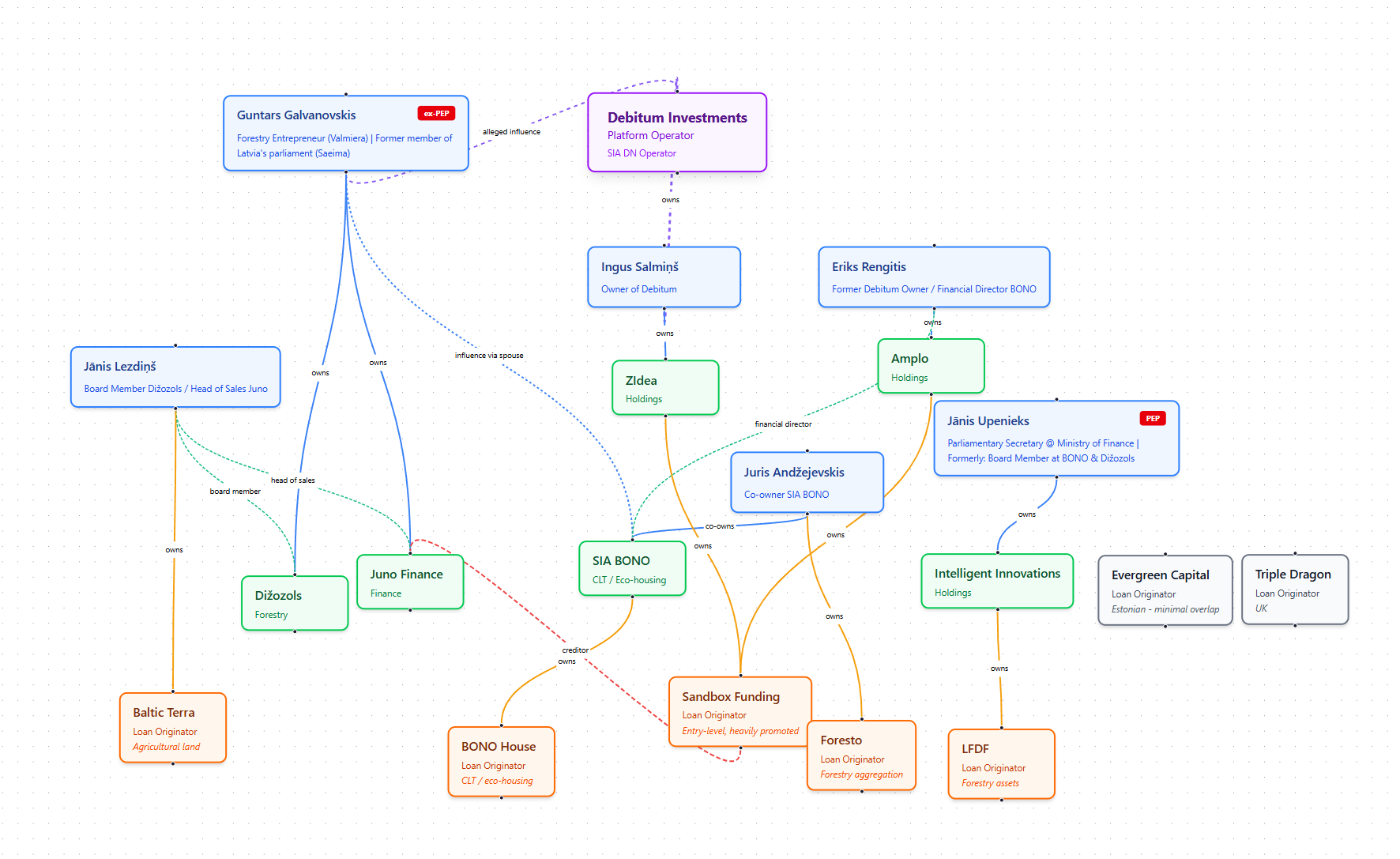

Internal Lenders

The following overview summarizes publicly available information about selected internal lenders funded via Debitum:

Sandbox Funding

- Owned by ZIdea (Ingus Salmiņš) and Amplo (Eriks Rengitis)

- Previously owned by WIN WIN INVESTMENTS (Henrijs Jansons)

- Largest creditor of Juno Finance

- Heavily promoted on Debitum

Baltic Terra

- Owned by Jānis Lezdiņš

- Agricultural land strategy

- Personnel overlap with the Dižozols ecosystem

BONO House

- Owned by SIA BONO

- CLT / eco-housing projects

- Valmiera-centric exposure

Foresto

- Owned by Juris Andžejevskis

- Forestry aggregation fund concept

- Part of the same regional / people cluster

Juno Finance

- Owned by Guntars Galvanovskis

- Largest creditor: Sandbox Funding

- Sales linked to Jānis Lezdiņš

LFDF (Latvian Forest Development Fund)

- Linked to Jānis Upenieks

- Forestry asset exposure

- Historical overlap with the BONO ecosystem

Here is a visualization of the management overlap between the mentioned companies.

Key Risk Considerations

High sector concentration risk

A large share of investor capital appears exposed to a single economic cluster centered on forestry, land, and construction. That increases sensitivity to sector-specific downturns.

Geographic concentration

Many internal lenders operate in the same regional ecosystem. This can amplify local economic, regulatory, or liquidity shocks.

Interconnected counterparties

Overlapping ownership, management, and creditor links can increase correlation risk. Stress in one entity may affect several others at the same time.

Limited diversification despite multiple issuers

Although capital is spread across several issuers, the underlying economic exposure may be less diversified than it first appears.

Refinancing and capital recycling dependency

In closely connected ecosystems, refinancing activity may play a larger role in maintaining loan flow. That can become a weakness during periods of market stress.

Based on our research, we contacted Debitum directly. The platform’s responses were coherent, detailed, and broadly consistent with the structural picture we identified. We found no evidence of undisclosed ownership or regulatory evasion. However, the current setup still requires investors to actively interpret prospectuses and structural relationships rather than relying on surface-level diversification signals.

Is Debitum Safe?

Debitum is regulated, but regulation should not be confused with low risk. The key issue is not whether the platform operates legally. The key issue is whether the investor understands how concentrated and interconnected the current exposure may be.

For investors who want broad diversification across unrelated lenders, sectors, and geographies, Debitum may not be a good fit. For investors who are comfortable underwriting a narrower and more correlated regional ecosystem, the platform may still be relevant as a higher-risk allocation.

Origins and Legacy Issues

Debitum Network was founded by three Co-Founders Martins Libert, Donatas Juodelis and Justas Šaltinis.

All of them are connected to the Latvian factoring company Factris, which acquired another invoicing company Debifo back at the beginning of 2019.

According to the LinkedIn profiles of the co-founders Donatas Juodelis and Justas Saltinis, they are no longer active in developing the Debitum Network.

The three co-founders raised USD 17.2M in Ethereum via a token generation event by issuing the so-called DEB token, intended to provide users with potential returns.

Shortly after the issuance, the co-founders converted the raised crypto into fiat and used the funds to develop the platform. None of the backers have ever seen a refund or benefited from the DEB token, which essentially funded the platform.

The original management has not disclosed how the funds have been used. Based on our knowledge, a platform like Debitum Network didn't cost millions to develop.

Debitum's ICO and the DEB Token

Experienced investors may recall that Debitum Network participated in a Token Generation Event (TGE) in which the platform sold DEB Tokens, a utility token, to contributors. The funds raised from this event were intended to build the platform and expand the business.

According to Debitum’s whitepaper, the platform was designed to address the credit gap for small and medium-sized enterprises (SMEs). The founder has confirmed that this goal remains a priority for the platform.

For more details about the Initial Coin Offering (ICO) and the intended utility of the DEB token, we recommend watching our full P2P talk. At the 13:45 mark, the former CEO stated that the platform raised nearly $18 million to develop it. At mark 15:48 the founder explained that the raised funds were used to build the platform, cover marketing and business development expenses.

The CEO also committed to further enhancing the utility of the DEB token—a promise that was ultimately not fulfilled.

Current Leadership

In 2023, the company was sold from the previous management to Mr. Rengitis. During the transaction, the management ensured that any trace of the DEB token would be erased to cover the ICO pursued by the initial founders.

As of 2026, Ingus Salmiņš is the owner and CEO of the Debitum platform.

Bottom Line

Debitum is easier to use and more regulated than many platforms in the sector. But regulation alone does not offset the current structural risks.

The main concern is concentration. Much of the portfolio appears tied to one regional ecosystem, one sector cluster, and several interconnected counterparties.

That does not make Debitum uninvestable by definition, but it does make the platform unsuitable for conservative investors seeking broad and transparent diversification.

If you invest through Debitum, you should do so with full awareness that multiple issuers do not necessarily mean multiple independent risk sources.

Debitum Alternatives

Debitum is not the best fit for risk-cautious investors. If you prefer clearer structures or broader diversification, there are alternatives worth considering.

Fintown

Fintown is a Czech-based crowdfunding platform raising funds to refinance the equity of the Vihorev Group, which is developing rental properties in Prague. If you invest in operational rental properties, you can expect monthly rental income, increasing your cash flow from P2P loans.

Learn more in our Fintown review.

Nectaro

Nectaro is a regulated P2P lending platform based in Latvia, offering investments in loans from Moldova and Romania. With loan terms ranging from 2 to 5 years, Nectaro offers greater loan availability than some other platforms. All loans are backed by a buyback obligation, offering an added layer of security for investors.

Learn more in our Nectaro review.

Indemo

Indemo is a regulated Latvian crowdlending platform offering investments in discounted Spanish debt with a minimum expected return of 15% and a lock-up period of at least 2 years. The platform provides a unique concept in the industry, while so far delivering above-average returns for the community.

Their business model is more straightforward, and based on the key information sheet, the risk profile appears easier to understand than Debitum’s current structure.

Read our Indemo review to learn more.